In a recent item, I concluded — based on my analysis of an email exchange between former Fortune reporter Bethany McLean and Copper River Partners (formerly known as Rocker Partners) — that McLean wrote a highly critical article about Fairfax Financial Holdings (NYSE:FFH) with the expectation that her work would cause FFH stock to drop precipitously in value.

By way of review, the evidence shows that a manager of Rocker Partners hedge fund first approached Bethany McLean about Fairfax on December 7, 2006. Bethany then met with Rocker Partners employee (and former SEC attorney) Richard Sauer 11 days later, and presumably began work on what would become her March 6, 2007 article The inside story of a Wall Street battle royal shortly thereafter.

The evidence further demonstrates that when, by March 21, 2007, FFH stock price had gone up 45 points instead of down as expected, McLean was unhappy.

Why would this be?

Anybody familiar with the ongoing conversation held on this blog knows the answer, but not wanting to take for granted that all readers here are either sufficiently seasoned or in agreement, I offer the following, which was, like the above-referenced email exchange, gleaned from the many documents gained through discovery in the Fairfax Financial vs. SAC Capital, et al, lawsuit; specifically, from records of Rocker’s evolving short position in Fairfax stock during the months before and after the publication of McLean’s article.

Beginning on January 4, 2007: ten trading days after McLean met with Richard Sauer, Rocker Partners shorted $2.4-million in Fairfax stock.

In February, Rocker added just over $100,000 to their Fairfax short.

Then, on March 1, 2007, three trading days before McLean’s article, Rocker added another $1.5-million to their position.

All told, Rocker was betting at least $4-million that the price of Fairfax stock would drop.

But unfortunately for Rocker, that’s not what happened.

Indeed, Fairfax stock rose a healthy 20% between March 6th and 22nd, when Rocker’s partner emailed McLean, wondering why Fairfax wasn’t dropping as a result of her story, as expected.

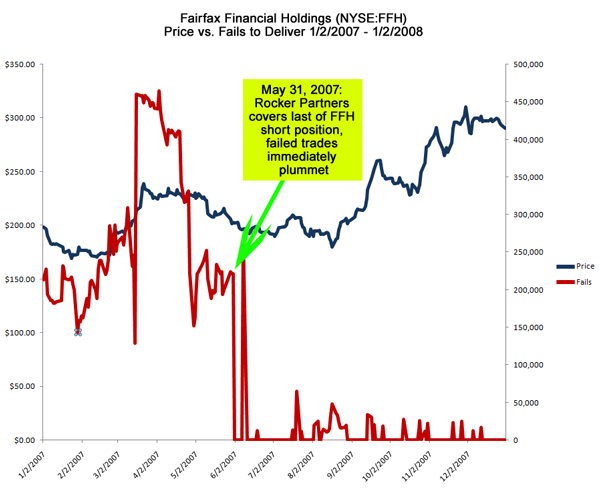

Apparently satisfied that circumstances were unlikely to improve, that very day Rocker began covering its short position…97,000 shares worth, to be exact. By the end of May, Rocker’s entire Fairfax short position was closed out, at a substantial loss.

Of course that’s all interesting, but as always, there’s more.

An analysis of the failed trades in Fairfax stock recorded and disclosed by the SEC for that period proves instructive.

Most notable is the sharp decline in FFH failures to deliver observed at the end of May, 2007. In fact, with the exception of a transient spike on June 8, fails are essentially reduced to zero at precisely the same time Rocker Partners closes out its FFH short position.

Given such a deep commitment to cheating, I find it surprising Rocker Partners never managed to be a more successful hedge fund.

If this article concerns you, and you wish to help, then:

1) email it to a dozen friends;

2) go here for additional suggestions: “So You Say You Want a Revolution?“

. . . the information is just becoming available to turn the table on everyone from the SEC on down . . .

. . . my question has always been damages and how to distribute them. I think there is a way to do this that is objective and not subjective. More next year.

Best to all for the holidays.

AMG

do you think Naked Short sellers had the same game plan? Maybe they could not get Mclean but used a 2nd team player Like Carol R. to help knock down the stock price to profit. How many times do you think this was used? looks to me they used it 50 times each on TASR, OSTK, CALM, NFLX, DNDN. FRPT just to start.

C’mon Judd, its a reach.

The SEC report reads that at precisely the same time Rocker covered his legitametly hypothecated short, a little old lady in Pasedena who had been searching desperately for a lost 97,000 share Fairfax certificate she has soldweek ago, finally found it, and delivered it to her broker who had been extremely understanding and patient waiting for the stock from this retail sale. Further, Bethany had done exhausting digging, interviews, and research to arrive at her conslusions for the stories. She was disgusted it did not drop in price because she honstly believes she is part of the fourth estate, and trying to protect those who traded in food stamps to purchase Fairfax.

By the way, the report was written in crayon.

Judd,

There were considerable fails before these transactions. How do you account for them? If the options data showed puts outstanding, was the OMM hedging by not delivering? When the transactions occurred, was there an increase in outstanding puts because the fails increased almost twice the 97K shares mentioned between Jan at 250K and 450K at the peak. The fails to deliver are consistent with the OMM covering 250K shares coinciding with the end of the position or another party that is trading the same way in concert. Are there any emails between other traders from the hedge fund during this period?

Judd,

Can you tell me who uses the Yahoo name >> captainblood2000 <<

Thanks.

I’m pretty curious about a particular Yahoo user too. The main alias is “ecd.fan”, though there are several others this individual is suspected of using. He has a particularly insidious interest in dragging down Energy Conversion Devices, which itself has spent some time on the RegSho list. I’d appreciate it if your offer to run names through the DSA still stands.

A little research on ECD.Fan’s identity…

From EDN News on PCM chips – I’ve talked to Todor Mitev before when he was trying to “advise” a previous Solar employer of mine.

—

http://www.edn.com/blog/980000298/post/1620047762.html

—

For more on ECD.Fan, contact Todor Mitev.

Todor Mitev

Temujin Fund

140 Broadway, 38th Floor

New York, NY 10005

212-299-5446

[email protected], or

[email protected]

He may know ECD fan personally. He might even see him daily.

—

(cached version from Google)

http://74.125.47.132/search?q=cache:XDRol2XxsvcJ:www.edn.com/blog/980000298/post/1620047762.html+ecd.fan+todor+mitev&cd=2&hl=en&ct=clnk&gl=us&client=firefox-a

Looks like the racketeers are showing up here as well to defend their accomplices. As to the Yahoo message forums; the paid bashing is so overwhelmingly evident it is simply undeniable. Although there are always exceptions, notice that bashing is most prominent during hours that the market is open (and a bit into after hours trading as well). I am currently watching the stock American Capital Strategies (ACAS) that has been hammered by naked shorts and spent a very very long time on the REG SHO list. The company had to suspend the dividend to conserve capital, and now the shorts have smelled blood and the Milberg-Weiss class actions have begun. The Yahoo message forum is overwhelmed by obvious bashers who have no other reason to be sitting there day in and day out during regular business hours, unless they are actually being paid to do it.

It is incredibly frustrating to decent investors.

http://seekingalpha.com/article/111852-will-comex-default-on-gold-and-silver

Now, however, because of the premiums available in the real market, buying a futures contract and demanding physical delivery upon maturity has become a cheap method of obtaining substantial quantities of physical gold and silver. With respect to the December contract, for example, exchange records show that more than 5% of people holding open standard sized (100 ounce) gold futures contracts, and about 10% holding open silver futures contracts (5,000 ounce) demanded delivery. The delivery demands are happening even more often among deliverable mini-contracts (33.2 ounce gold/1,000 ounce silver) purchased on the NYSE-Liffe exchange.

Some speculate that clearing members of the exchanges, who have sold gold and silver short on the futures market, will eventually be bankrupted by these delivery demands. According to these skeptics, the gold and silver consists mostly of fake claims to vaulted supplies that do not exist. They say that futures contracts are nothing more than “fake paper gold” and most refuse to buy on the futures markets, opting, instead, to pay huge premiums at retail gold and silver dealers. The skeptics may be right about the failure to keep adequate supplies of vaulted metal, but it doesn’t really matter. If you buy gold and silver on the futures exchanges, you will get your metal, whether or not the short sellers are trying to defraud you, and I’ll now explain why.

I can’t help thinking that with Buffett’s relationship to Patrick and Buffet’s support of the Obama campaign, that there is going to be some serious reckoning coming in February.

If I was a bad guy, I’d be making deals today to sell out my partners in crime.

The Cramer’s, McLean’s and Greenberg’s of the world, who put their faces to supporting this crime are going to face the pitchforks and torches of us commoners come 2009.

Mhelburn: There were substantial fails before the year reflected in the graph. September 15, 2006, for example, saw 1,200,000 failed trades — which was much more than double the real volume for the day.

One gets the impression that by late 2006, Rocker was operating independent of the other hedge funds (in contrast with the period from 2002-2006, during which they were working closely with Third Point, Kynikos and Exis).

I suspect Rocker’s strategy was to flood the market with fails as a strategy for supporting his legitimate short positions. Once he had covered the last of his shorts, there was no reason to continue naked shorting, and so the fails stopped.

Get ready for Civil Unrest !! Lets ( Washington Crooks) Reward the Crooks (Hedge Funds) with “OUR” (US Taxpayers) Money.

Hedge funds gain access to $200bn Fed aid

By Krishna Guha in Washington

December 20, 2008 6:01:44 AM

Hedge funds will be allowed to borrow from the Federal Reserve for the first time under a landmark $200bn programme intended to support consumer credit.

The Fed said on Friday it would offer low-cost three-year funding to any US company investing in securitised consumer loans under the Term Asset-backed Securities Loan Facility (TALF). This includes hedge funds, which have never been able to borrow from the US central bank before, although the Fed may not permit hedge funds to use offshore vehicles to conduct the transactions.

The asset-backed securities to be funded under the programme are pools of credit card receivables, automobile loans and student loans.

The idea is to increase the supply of these loans and reduce borrowing rates by ensuring that the companies that make the loans can sell them on to investors who have guaranteed access to low-cost funding from the Fed.

The TALF is a key plank of the unorthodox strategy set out by the Fed last week as it cut interest rates virtually to zero. Washington insiders expect the programme will be dramatically expanded next year with further capital support from Treasury once the Obama administration takes office.

A senior official in the outgoing Bush administration told the Financial Times it could also be broadened to include new commercial and residential mortgage-backed securities.

The Fed thinks risk premiums or “spreads” for consumer loans are much higher than would be justified by likely default rates, even assuming a nasty recession.

It attributes this to a lack of buying interest in the secondary market where the loans are sold on to investors. By making loans to these investors on attractive terms it aims to increase market liquidity.

Making the scheme open to all US companies is a radical departure for the Fed, which normally supports financial market liquidity indirectly by ensuring banks have adequate liquidity to make loans to other investors.

However, the liquidity the Fed is providing to banks is not flowing through to financial markets, because banks are balance-sheet constrained and risk-averse. So it is channelling funds directly to investors.

The scheme is not designed specifically for hedge funds and a wide range of financial institutions are likely to participate.

Nonetheless, Fed officials hope that hedge funds will be among those investors that take advantage of the low-cost finance to drive down spreads.

The loans will be secured only against the securities and not the borrower. However, the Fed will lend slightly less than the value of the securities pledged as collateral. The Treasury has committed $20bn to cover potential losses.

Since the credit crisis erupted, hedge funds have complained that they cannot get the leverage they need to arbitrage away excessive spreads and meet high hurdle rates of return.

“Demand is there for leverage but not supply,” said Sylvan Chackman, head of global equity financing at Merrill Lynch.

In effect, the Fed will now take on the role of prime broker – the lead bank that lends to a hedge fund – for specific assets.

Additional reporting by Henny Sender in New York

This was submitted to the SEC in 2005…

http://online.wsj.com/documents/Madoff_SECdocs_20081217.pdf

For those that don’t read the link, this guy (a derivatives expert trading billions of dollars) has been anonymously complaining to the SEC that Madoff is a Ponzi scheme since 1999 and he notes that the auditing firm is run by Madoff’s brother in law and by having senior roles on the DTCC board of directors and a founding member of the European clearing system, he’s not being properly monitored.

Since most here recognize the yahoo message board is used by paid bashers the question begs why isn’t yahoo’s terms and agreements adhered? Is yahoo complicit? Since some are presenting names. How about RayStock48 that is now active with GE, was active with SNDK and JAVA. Looked like one name with multiple users.Does that TACTIC sound familar? So once again it’s nice to KNOW the problems. That’s easy. It’s how do we get to the solutions and also subject those who are complicit accountable. Most know the names.

Where are the rest of the shareholders like this one??

STOCKS NEWS US-Madoff victim files claim against SEC: WSJ

Tue Dec 23, 2008 12:20pm GMT Email | Print | Share| Single Page | Recommend (0) [-] Text [+]

Market News

STOCKS NEWS US-Markets modestly higher after weak housing data

STOCKS NEWS US-Option players eye Zions Bancorp puts

STOCKS NEWS EUROPE-Beta Systems up on planned acquisition

More Business & Investing News… Stocks on the move [HOT-RTRS] Real-Time Equity news [U E]

U.S. stock market report [.N] 0715 ET 23Dec2008-Madoff victim files claim against SEC: WSJ ——————————————————————————

Phyllis Molchatsky, an investor who lost nearly $2 million by investing with Bernard Madoff, has filed a claim against the Securities and Exchange Commission alleging that the agency was negligent in failing to detect an alleged fraud, according to a report in the Wall Street Journal. Molchatsky is seeking $1.7 million in damages. [ID:nBNG153505]

Reuters Messaging: [email protected] 0707 ET 23Dec2008-Firm sees first-ever fall in solar panel revenue ——————————————————————————

Madoff Fund Operator De La Villehuchet Found Dead in Suicide

By Saijel Kishan, Katherine Burton and Henry Goldman

Dec. 23 (Bloomberg) — Thierry Magon de La Villehuchet, who ran a fund that invested with Bernard Madoff, was found dead today in his New York office in an apparent suicide, Police Commissioner Raymond Kelly said.

“Our investigative premise is that it was a suicide,” Kelly said in an interview. De La Villehuchet, 65, was found “with his feet propped up on his desk, a trash pail nearby to collect blood,” and no sign of a second person, Kelly said.

The money manager had “multiple stab wounds” to his arms and wrists, a box-cutter and pills were found nearby, and no suicide note was found, Kelly said. De La Villehuchet was co- founder and chief executive officer of Access International Advisors, a New York firm that invested $1.4 billion with Madoff, who was arrested on Dec. 11 for allegedly running a $50 billion Ponzi scheme.

The death of de la Villehuchet, who founded Access in 1994 with Patrick Littaye, came as lawsuits mounted in connection with investors victimized by Madoff. Fairfield Greenwich Group, a hedge-fund firm that had $7.5 billion invested with Madoff, has been sued by investors for allegedly failing to protect their assets. A New York woman who says she lost most of her savings is seeking $7 million in damages from the Securities and Exchange Commission for Madoff losses.

The tally of investors hurt by Madoff continues to grow. Pedro Almodovar, the Spanish film director known for movies such as “Women on the Verge of a Nervous Breakdown” has about $280,000 at risk, El Economista reported.

Credit Lyonnais

De La Villehuchet was chairman and CEO of Credit Lyonnais Securities USA, the U.S. investment banking arm of the French bank, according to Access marketing documents. Prior to joining Credit Lyonnais in 1987, he ran Interfinance, an international broker firm specializing in French, Belgian and Italian stock markets that he founded in 1983.

Access managed $3 billion and had 26 employees according to marketing documents dated September, and its LUXALPHA SICAV- American Selection fund invested solely with Madoff. Access said last week that it was working with lawyers to assess the situation. UBS AG was LUXALPHA’s administrator until this year, and is no longer involved with it, said Karina Byrne, a UBS spokeswoman.

Clients of Madoff had at least $36 billion with his firm, according to a Bloomberg tally that may include some double counting. Before his arrest, Madoff, 70, confessed to employees that his “giant Ponzi scheme” may have cost as much as $50 billion, according to an FBI complaint.

His misconduct may have stretched back to at least the 1970s, two people familiar with the government’s inquiry of Madoff said last week. Madoff is now under house arrest at his New York apartment.

To contact the reporters on this story: Saijel Kishan in New York at [email protected] Burton in New York at [email protected]

(I think if the student of abusive naked short selling (ANSS) can get a grasp of WHY the SEC acts like it does then the pandemic nature of the fraud can be better appreciated. This is a snip-it of an interview with Matt Renner-the interviewer and Gary Aguirre-the interviewee. Gary is an Ex-SEC lawyer that was “mysteriously” fired after going after a Wall Street “whale” for securities laws violations. Note the “revolving door” analogy and the “just don’t rock the boat” mentality for SEC staff. If you “just don’t rock the boat” by prosecuting Wall Street big fish then you will have your turn to go through the “revolving door” from the SEC to jobs on Wall Street paying 10 times as much. Why are they worth paying that much money annually? It might partly be for previous “favors rendered” but mainly because of the contacts they have that are still within the SEC and that can be tapped for “favors” when in need i.e. for willingly donning a blindfold when the ex-SEC staff member’s new employer’s actions fall under the microscope. This mentality explains a great deal about the SEC’s behavior when it comes to the refusal to provide truly meaningful deterrence to abusive naked short selling crimes as this might “rock the boat” of the hand that may soon be feeding you.)

MR: Why do you think the SEC didn’t use these regulatory powers (over “investment advisors like Bernie Madoff) in this (Madoff) case?

GA: We can’t really prejudge it at this point. There is a lot of talk in the media that there were personal links between SEC staff and Madoff. One has been identified; I’m not sure he was the only one involved. But stepping beyond personal connections, in general, I believe that the SEC has been reluctant to apply the securities laws to the big players, to Wall Street’s elite. They have often gotten a pass. The SEC is focused on the small players.

In the investigation that I conducted (on a Wall Street “whale”), which is now the subject of a Senate report, there was suspicious trading activity involving both a hedge fund involving an $18 million profit. They also detected a $150,000 profit by a low-level employee of General Electric (GE) and a Taiwanese kung fu instructor. SEC passed on the hedge fund case where the trading indicated millions in profit and SEC focused on the GE employee and the kung fu instructor. The SEC and the US attorney rigorously prosecuted the low-level GE employee, but both passed on any investigation of the major hedge fund.

This is not a rarity; it is more the practice. The exception is when they look at an elite player on Wall Street. Not only is it an exception, if you try to pursue a big player as I did; it can be career-shortening experience. At the SEC, it is a culture of deference. That culture is intolerant of investigations into the Wall Street elite. Keep in mind that the SEC was created to keep an eye on Wall Street, so it has completely lost sight of its mission and that is why we have a situation like the one with Madoff.

MR: What is it about the culture at SEC that steers them away from looking at the big Wall Street players?

GA: All the agencies have to some extent or another a revolving door [where government employees rotate out to the private sector and earn more money]. But at the SEC, what you rotate into is an enormous salary leap. SEC managers may make $200,000. That same person may make $2 million as a starting salary on the outside and can move up from there. Now, when he leaves, I’m not sure he’s worth $2 million as a lawyer, but he takes his Rolodex with him and that Rolodex is gold. The system maintains itself, because those that stay know their turn will come if they play the game. They see a director or associate director move onto a $2 million job with a Wall Street law firm. Then, the departed employee calls back to his former colleagues and says, “you know I really don’t think there is much of a case against so-and-so, I’d like for you to take a look at it.” And the case goes away; the system goes on in perpetuity.

MR: Did you see the revolving door in action in your case?

(On January 31, 2005, prior to the phone call mentioned below, an email beginning with the word “Yowza!” was sent from Jan Lower, an attorney at the Debevoise and Plimpton law firm, to Aguirre’s supervisor Paul Burger. The email described in detail the potential earnings that a former SEC official could receive at the Debevoise and Plimpton law firm – $2 million a year.)

GA: Senior officials at the SEC got a call from Debevoise lawyer asking about a case I was handling. It was clear she wanted the investigation of John Mack to go away so he could become Morgan Stanley’s new CEO. And it did go away. SEC associate director Paul Berger derailed the investigation and when I questioned that decision, fired me. Within a few days of firing me, he made an inquiry through one of his colleagues to the Debevoise law firm to see if they were interested in hiring him. After the case against Mack was dead, Berger took a job with Debevoise and that is where he’s working now. I’ll let you draw your own inferences.

What you have when you leave the SEC is contacts with the SEC, you have the Rolodex and the ability to call back to people you used to work with. I don’t want to single out Burger, I think that is really the culture there. A culture of ‘don’t rock the boat,’ the industry does not want ‘boy scouts,’ and if you can be effective with the SEC through your contacts, that is a very valuable asset you can bring to the table.

and who pays for these exorbitant salaries? Debevoise clients…and how do they get the money to pay these exorbitant salaries and bonuses? Oh, wait, they take bailout money from us to pay Debevoise to pay Paul Berger after he fires Gary Aguirre…

Got it

How come this bigger Ponzi scheme isn’t getting any press?

http://www.nypost.com/seven/12042008/business/ponzi_scheme_at_citi_142511.htm

Patchie post in 2006

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=34210816

kevin,

Maybe the press is captured ? lol

Say it ain’t so !

Kevin, It makes you wonder what lurks within Knight and UBS, the other pro counterfeiting letter writers.

Knight has a fund named Deephaven.

We need to do what we can to make all the Ponzi schemes fail as soon as possible as the snowflakes have been piling and there is an avalanche of CHANGE coming in the new year.

It’s going to be torches and pitchforks for the mouthpieces of the captured media come 2009.

NEW YORK, Oct 30 (Reuters) – Knight Capital Group Inc (NITE.O), the electronic trading services provider, said its Deephaven Capital Management LLC unit has suspended withdrawals from two hedge funds, including its flagship, after investors demanded much of their money back.

http://www.reuters.com/article/regulatoryNewsFinancialServicesAndRealEstate/idUSN3053834020081030

I can’t help but think the ladies doth protest too much. The ones that freaked out the most and wanted grandfathering and other protections are the ones that are likely guilty.

“Top wholesalers Knight Capital Group, UBS Securities and Bernard L. Madoff Investment Securities are voicing their concerns in letters and in public forums over an SEC proposal to scrap an exception to Regulation SHO.”

A lot of these fund managers that fail to deliver / counterfeit everything from stock to grain to oil to gold have an achilles tendon.

They are extremely vulnerable to the danger their own investors ever realize it’s a ponzi scheme and the reason no counterfeiters live on Park Avenue is you can be right 1,000 times, but that last time bankrupts you when you are wrong.

It’s easy to create a run on the scumbag’s “bank”.

The louder we can scream and the more light we can shine on these cochroaches and the more rocks we can overturn, the more quickly they will be gone.

http://business.theglobeandmail.com/servlet/story/RTGAM.20081212.wubsfund1212/BNStory/SpecialEvents2/home

http://www.propertyweek.com/story.asp?sectioncode=36&storycode=3130161&c=1

It’s snowing tonight and I can’t help looking at the window and watching the snowflakes land. Just like individual efforts, which seem to be frustratingly slow in bringing change, the snowflakes pile up as the letters do.

The avalanche of change is coming in early 2009.

Why is Madoff not in jail?

Maybe they hope he will take a dive out his window or someone will get a bead on him with a hand cannon.

Could that save someone some trouble?

Yes Ron,

I believe they put a bulls eye on him so he will never make it to testify against those who had knowledge. In the past, many who had information on other elite died from self inflicted gun shot wounds to the “BACK OF THEIR HEADS.”

A lot of people being suicided around Madoff already…

Like Gary Webb, a few years ago, who shot himself in the head, twice. Suicide, ya, sure.

He was rumored to be investigating the role of Wallstreet and drugs. He’s the one who revealed the CIA’s role in bringing drugs in for Iran Contra.

Can anyone point me to a website where the history of when Congress enacted laws to make hedge funds unregulated is explained?

I am beginning my generic letter to Congress (which I will post here) and would like understand the history of how hedge funds were made UNREGULATED by Congress.

iStandUP…start here, but much is found by a google search:

http://www.investopedia.com/articles/mutualfund/05/HedgeFundHist.asp

A Brief History Of The Hedge Fund

by Jim McWhinney (Contact Author | Biography)

Story Tools

Famed hedge fund manager Mario Gabelli wrote in 2002: “Today, if asked to define a hedge fund, I suspect most folks would characterize it as a highly speculative vehicle for unwitting fat cats and careless financial institutions to lose their shirts.” This characterization stems from the hedge fund’s recent history, which began with the headline-making collapse of Long Term Capital Management in 1998 and continued with the sensational meltdown of the Tiger Funds in March of 2000, followed by the reorganization of the once high-flying Quantum Fund in April of 2000. These high-profile incidents overshadow more than half a century of hedge fund history that began when Alfred Winslow Jones launched the first hedge fund in 1949.

The Father of the Hedge Fund

Alfred Jones was born in Melbourne, Australia in 1901 to American parents. He moved to the United States as a young child, graduated from Harvard in 1923 and became a U.S. diplomat in the early 1930s, working in Berlin, Germany. He earned a PhD in sociology from Columbia University and joined the editorial staff at Fortune magazine in the early 1940s.

It was while writing an article about current investment trends for Fortune in 1948 that Jones was inspired to try his hand at managing money. He raised $100,000 (including $40,000 out of his own pocket) and set forth to try to minimize the risk in holding long-term stock positions by short selling other stocks. This investing innovation is now referred to as the classic long/short equities model. Jones also employed leverage in an effort to enhance returns.

In 1952, Jones altered the structure of his investment vehicle, converting it from a general partnership to a limited partnership and adding a 20% incentive fee as compensation for the managing partner. As the first money manager to combine short selling, the use of leverage, shared risk through a partnership with other investors and a compensation system based on investment performance, Jones earned his place in investing history as the father of the hedge fund.

The Rise of the Industry

When a 1966 article in Fortune magazine highlighted an obscure investment that outperformed every mutual fund on the market by double-digit figures over the past year and by high double-digits over the last five years, the hedge fund industry was born. By 1968, there were some 140 hedge funds in operation.

In an effort to maximize returns, many funds turned away from Jones’ strategy, which focused on stock picking coupled with hedging, and chose instead to engage in riskier strategies based on long-term leverage. These tactics led to heavy losses in 1969-70, followed by a number of hedge fund closures during the bear market of 1973-74.

The industry was relatively quiet for more than two decades, until a 1986 article in Institutional Investor touted the double-digit performance of Julian Robertson’s Tiger Fund. With a high-flying hedge fund once again capturing the public’s attention with its stellar performance, investors flocked to an industry that now offered thousands of funds and an ever-increasing array of exotic strategies, including currency trading and derivatives such as futures and options.

High-profile money managers deserted the traditional mutual fund industry in droves in the early 1990s, seeking fame and fortune as hedge fund managers. Unfortunately, history repeated itself in the late 1990s and into the early 2000s as a number of high-profile hedge funds, including Robertson’s, failed in spectacular fashion.

The Hedge Fund Today

With media attention still focused on the recent failure of some hedge funds, there has been an increasing move towards their regulation. In 2004, the Securities and Exchange Commission adopted changes that require hedge fund managers and sponsors to register as investment advisors under the Investment Advisor’s Act of 1940. This greatly increases the number of requirements placed on hedge funds, including keeping up-to-date performance records, hiring a compliance officer and creating a code of ethics. All hedge funds that fall under the new SEC rules must be registered by Feb 1, 2006. This is seen as an important move in protecting investors. (For more information, see the SEC website.)

Despite troubles in the last few years, the hedge fund industry continues to thrive. The development of the “fund of funds”, which is simplistically defined as a mutual fund that invests in multiple hedge funds, provided greater diversification for investors’ portfolios and reduced the minimum investment requirement to as low as $25,000. The introduction of the fund of funds not only took some of the risk out of hedge fund investing, but also made the product more accessible to the average investor.

Conclusion

Hedge funds have evolved significantly since 1949. Modern hedge funds offer a variety of strategies, including many that do not involve traditional hedging techniques. The industry has also rapidly grown, with recent estimations pegging its size at $1 trillion – quite the leap from the $100,000 used to start the first fund half a century ago.

With a fascinating past that has twice seen media-fostered publicity push the industry to stratospheric highs and vilify it when it fell from grace, it seems highly probable that the cycle will repeat itself at some point in the future. While it is easy to get sucked in by the hype or repelled by the negative press, it’s always advisable to take a step back and conduct some due diligence, just as you would prior to making any investment. Take the time to learn more about hedge funds – for example, you may want to start by reading our Introduction to Hedge Funds – Part 1 and Part 2.

Before you put your hard-earned money at risk, you have to make sure you are choosing the right investment for the right reason. Don’t blindly chase performance, and remember that past performance is not an indicator of future performance.

iStandUp..

and this:

http://www.law.harvard.edu/programs/olin_center/corporate_governance/papers/Brudney2008_Horsfield-Bradbury.pdf

Davidn may be onto something regarding exposing other Ponzi schemes.

I’m glad they are going after Stevie Cohen, but they should go after Knight Deephaven and UBS, the other two besides Madoff the begged for the grandfather clause

http://tinyurl.com/8udj6k

The second-biggest investor in hedge funds will demand that some of the largest names in the industry, including Cerberus, Citadel, DE Shaw and SAC Capital, appoint independent administrators or face it pulling its money.

Switzerland’s Union Bancaire Privée, in an internal memo, instructed managers of the $56bn it has allocated to hedge funds to put in immediate redemptions for any fund that does not have independent administrators and custodians, following its heavy losses from the alleged fraud by Bernard Madoff.

…

Webmaster’s Commentary:

This may force some new Ponzis into the light!

(from http://www.whatreallyhappened.com)

For the captured media, the 18th most censored story of 2006. Every media reporter is sent copies of top censored stories, so they all knew about it.

I know for a fact that this went to the commissioners at the SEC in 2006.

“Little Known Stock Fraud Could Weaken U.S. Economy”

http://www.projectcensored.org/top-stories/articles/18-little-known-stock-fraud-could-weaken-us-economy/

“As short-selling is a sale of stocks not owned, but loaned, it is an example of buying on margin-a category of practices whose abuses stand out clearly in many people’s minds as a significant factor in the Stock Market Crash of 1929 which ushered in the Great Depression”

The last link concerns me as 2009 has the potential to be worse than 1929 eighty years ago.

A little girl tried selling me lottery tickets that were on sale. Last year, they were $1 each, but now they were 5 for a dollar. I smiled, because your odds are exactly the same. If everyone has five times as many tickets, your $1 purchase buys you exactly the same amount of chances.

That’s where we are today. A dollar represents your share of the economy. which is currently $13.13 trillion. If they doubled the number of dollars outstanding, then shared them out pro rata, your share of the economy would be EXACTLY the same even though each dollar was worth half as much. You’d have twice as many of them.

We could be saved from 1929 by understanding this.

Let’s say, for instance, that they increased the supply of dollars by 20%, which would make every dollar 1/1.2 = 83% as much as it used to be. It wouldn’t matter as long as those new dollars were distributed pro rata. Every one would be exactly as wealthy as they were before this happened.

Unemployment causes people to be less wealthy. If only half the people were working, then the GDP would only be $6.565 trillion and all of our dollars would be worth half as much.

So, here’s what a lot of people have trouble wrapping their head around. If you print money and it keeps the economy from shrinking by keeping everyone employed and in their home and the money is distributed pro rata, then everyone has the same percentage of the national wealth and the national wealth doesn’t shrink and we all got something for free.

I’m a bit left leaning and would consider myself a Democrat, but here’s where tax cuts make sense. Obama could offer massive tax cuts (no capital gains, huge cuts in the brackets, etc.) which would allow people to keep their homes and employ other people and as long as he then monetized that debt, rather than borrow it from the privately owned Federal Reserve and other bankster families, it would cost us nothing and make us all wealthier in 2010.

Let the car companies go bankrupt. Let Wallstreet go bankrupt. Write checks to mainstreet and save the economy.

…things that make you go, huh….

Reporter101

Thank you for the links about the history of hedge funds!

Redwood, man, what do you want to know about ecd.fan? Why don’t you instead urge ENER’s management to finally answer the questions ecd.fan is asking? Or are you afraid of the truth?

Wow! I’m definately inspired to know that there are those out there that have their eyes open and are willing to risk all in order to try to get us back on track. The total lack of ethics on those who hold the purse strings is still unfathomable and a huge shock. I was embarrassed by the cowboy arrogance of the previous administration. Who would have thought the SEC and the Treasury Dept are so wraught with conflict of interest? Thank you, Patrick. You offer me hope that someone is actively working to keep the rest of us informed.

This is the most thorough and informative information I have found. I really enjoyed it.

Keep working ,remarkable job! http://www.apnatorrents.com/download-mockingjay-the-final-book-of-the-hunger-games-pdf.html

วานนี้ โพสต์ เป็น ดี , น้องสาว คือการวิเคราะห์ ดังกล่าว ประเภทนี้

สิ่ง จึง ฉันจะ บอก แจ้ง เธอ .

Thanks for another informative web site. Where else may I am getting that kind of information written in such a perfect way? I have a mission that I’m simply now running on, and I’ve been on the glance out for such information.

Thanks!