Among the disturbing facts contained in the recently unsealed documents obtained via discovery in the Fairfax Financial (NYSE:FFH) vs. SAC Capital, et al, lawsuit are the lengths to which short-selling hedge funds go to attack the leadership of the companies they’ve designated for destruction.

In the case of Fairfax, when the work of corrupt Morgan Keegan stock analyst John Gwynn and thestreet.com columnist Peter Eavis failed to get the job done, a “real” expert was called in; namely: Spyro Contogouris of MI4 Reconnaissance.

In the case of Fairfax, when the work of corrupt Morgan Keegan stock analyst John Gwynn and thestreet.com columnist Peter Eavis failed to get the job done, a “real” expert was called in; namely: Spyro Contogouris of MI4 Reconnaissance.

Contogouris and MI4 employee Max Bernstein were hired by Exis Capital Management, among the smaller of the half-dozen hedge funds comprising the “Enterprise” targeting Fairfax, in early 2005. Their primary mission was to gain access to material non-public information from sources in and around Fairfax. Their secondary mission seems to have been harassment of Fairfax executives, both public and private.

This effort got off to an impressive start, in the form of a 30-page document anonymously sent by Bernstein to Rev. Barry Parker, head of the Toronto church attended by Fairfax CEO Prem Watsa. The gist of Bernstein’s package was as follows: Prem Watsa bears a striking resemblance to a convicted swindler named Marty Frankel, and even if Watsa is not Frankel, Rev. Parker should beware and call Watsa to repentance for Fairfax Financial’s accounting.

In December of 2005, Contogouris and Bernstein created premwatsa.com, an attack site. In one exchange of instant messages, the two discuss how to use posts planted on stock message boards to build traffic to the site, and blithely speculate as to how Watsa and other Fairfax officers will react upon discovering it.

Meanwhile, Contogouris created a document, since discredited, dubbed “Fairfax Fraud Facts”, which he circulated broadly among journalists and analysts. This document sparked substantial negative coverage of Fairfax.

It was possibly in this context that, in an undated instant messenger exchange, Andrew Heller, manager of Exis Capital, told Bernstein: “tell spyro, bloomberg was taken care of, and he will receive payment.”

I contacted Heller, seeking context to clarify this potentially significant tidbit, but he refused to comment, citing the ongoing nature of the Fairfax lawsuit. The only thing of any substance Heller would say was that his hedge fund remains “up net 15% on the year.”

Congratulations, Mr. Heller.

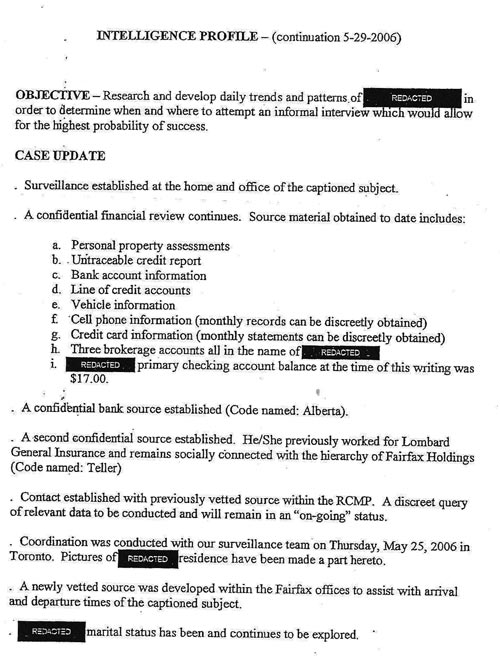

MI4’s effort to secure inside information ramped up significantly in May of 2006.

On the 29th of that month, MI4 created the following “Intelligence Profile” on an officer of Fairfax (whose name is redacted):

On May 31st, Contogouris, posing as a reporter, gained access to the back offices of that Advent Group, a Fairfax subsidiary in London, trolling for potential insiders to act as sources.

The next day, Contogouris personally delivered a package to Advent Group CFO Trevor Ambridge, asking that Ambridge provide inside information or risk criminal prosecution.

From his emails, one gets the impression that this is the sort of thing Contogouris quite relishes. However, presently things would take a rough turn for the self-styled corporate spy.

The first blow came six weeks later, when Fairfax named Contogouris in the lawsuit that led to the document production that led to this post.

The second, more severe blow came in November of 2006, when Contogouris was arrested by the FBI, charged (and subsequently indicted) with engaging in an unrelated multi-million-dollar real estate fraud.

While this came as a surprise to many, seasoned observers might have predicted something negative was about to happen to Contogouris when, in late September of 2006, apropos of nothing, Rocker Partners order-taker and former New York Post business writer Roddy Boyd, wrote FBI’S SECRET SOURCE, claiming:

“An FBI spokeswoman confirmed to The Post that Spyro Contogouris, who analyzes companies’ balance sheets, was deputized by the FBI in June to approach Fairfax’s former chief financial officer, Trevor Ambridge, as part of an investigation into the insurance company’s accounting and stock trading.”

It’s worth noting that none of the other writers following up on Boyd’s story — myself included — managed to get FBI confirmation of the supposed “deputy” status bestowed upon Contogouris.

In fact, the United States Senate Judiciary Committee found Boyd’s claim sufficiently strange to specifically ask FBI Director Robert Mueller about it, three weeks after Contogouris was arrested. Mueller’s response (see pages 70 and 71) was simple:

“The FBI does not “deputize” members of the general public.”

So what was motivating Boyd and Contogouris?

For Boyd’s part, that’s simple: as is revealed in documents unsealed in the Fairfax case reveal, (documents which I will be examining here shortly), Roddy writes what certain short-selling hedge funds tell him to write.

As for Contogouris, I suspect that, aware of the trouble looming on the real estate front, he made contact with the FBI as a “confidential informant” (something you or I could do at any time) seeking to ingratiate himself with that agency, possibly earning what he expected would be some form of immunity from other prosecution in the process. Then, fearing that despite these efforts his arrest was imminent, Contogouris used his hedge fund contacts to plant the story with Boyd, hoping the feds would be too embarrassed to nab someone they apparently trusted enough to “deputize”.

Four months after his arrest, the story of Spyro Contogouris and Fairfax was examined at length by another high profile business writer, who practically tied herself in a knot attempting to distance Contogouris from Fairfax’s attackers while simultaneously lending credibility to his work.

The author of that piece was none other than Bethany McLean.

To quote my friend Patrick Byrne: “If only there were a pattern.”

If this article concerns you, and you wish to help, then:

1) email it to a dozen friends;

2) go here for additional suggestions: “So You Say You Want a Revolution?“

Thank you for another Fantastic article!

You have done more to enlighten your readers to the corruption and manipulation in he marketplace than the NY Times, Washington Post, CNBC, Forbes, CNN, FOX, Wall Street Journal.. etc COMBINED! If Only the SEC would start to lock these crooks up for life.

I wish all of you and your families a very Merry Christmas and a Great New Year. Thank you for the work you are doing!

just might be the best Christmas gift I’ve ever received.

Thanks, Judd. Thanks!!!!!

thank you judd and merry merry merry christmas to you and your family.

be safe n warm

i think these creeps are runnin’ scared by now due to all the work by you and the team.

if there is anything i could do to help please ask.

take care

shawn

sender of exis…

http://cityfile.com/profiles/adam-sender

The more exposure the more we will be able to protect ourselves from these predators.

You are doing a service that is beyond anything the SEC has ever done and we are all on board. Keep it up!

The Loeb Awards are among the highest honors in journalism, recognizing the work of journalists whose contributions illuminate the world of business, finance and the economy for readers and viewers around the world.

Recipients mentioned in this expose… Nocera, Eavis, and McLean ….

They get awards for a specific article, so their constant bashing of stock doesn’t even hit the radar as far as the damage that they’ve been able to do.

Patrick ruffled feathers, and the media went into fortress mode… .. kinda like the Alamo. They have protected the worst among them and the professional comraderie and job hopping doesn’t seem to inspire real competition or honesty.

I noticed that Weiss and McLean are both writing at Conde; Portfolio and Vanity Fair. Now we can all go take a shower.

I stopped by Wiki and noted that overall, Patrick’s bio has been cleaned up and happened onto http://en.wikipedia.org/wiki/Intercollegiate_Studies_Institute This is an organization that works to stifle discourse as an agenda.

I loved the punchline of your blogpost: “If only there were a pattern.” Nice.

Merry Christmas, Deep Capture journalists!

mhelburn,

An interesting aside regarding the article on Adam Sender: It references his former relationship with film maker and activist Aaron Russo. Before his death, Russo disclosed that Nicholas Rockefeller had revealed to him prior knowledge of the September 11 attacks and the subsequent wars in Iraq and Afghanistan.

Unfortunately, youtube has recently made the videos of said interview private.

This is not a rabbit hole, it is an ant farm.

Merry Christmas, everybody.

Judd, please submit the facts to the department of justice. It is well past time for the miscreants to end up where they belong.

Judd,

I like the way that you have linked back in the comment section and these appear to be the last comment by you.

The intersection of mailing lists of Morgan Keegan and a list of customers of other analysts who allowed front-running would point a finger at those who were most apt to be using this as an investment strategy and most likely to be part of the larger cabal.

Great job Judd and a Merry Christmas to you and yours. Again, what a great job. I have a feeling that Roddy’s future is starting to look pretty bleak and Bethany better seek legal counsel after they throw her under the bus.I think it only fair to print pictures of Bethany and Roddy so that all might wish them a warm greeting when they see them. It is also very apparent that Roddy is no longer invited to speak at CNBC, which is just as well as he struggles very hard to spit out more than three words in a row. Sleep well Roddy, you looser.

http://ftp.sec.gov/rules/sro/nd9826/gorman2.htm

These 111 firms, including Madoff asked for the mm exemption in 1998. These firms are likely hiding spots for x-clearing fails.

How do the captured lapdogs talk about Madoff without mentioning failure to deliver?

It’s not a ponzi scheme. It’s a stock scam where new investors are paid from reduced collateral on fails from old investors.

From Madoff’s letter:

“One point in particular bears emphasizing: because the ability to sell short is critical to a market maker’s ability to provide liquidity and control its risk, the SEC and NASD must be careful to ensure that all market makers providing meaningful liquidity to the market are able to qualify as PMMs.”

Prediction:

Madoff will turn out to have been up to his keister in NSS.

Patrick

this fairfax discovery is the gift that just keeps on giving. big thanks to prem & company for standing up and making this possible. Just think boys and girls, we have ringside seats to the financial fraud story of the century, and very few know about it yet… but they will, and soon.

Pickled Shark,

In 2006, the NSS story was listed as no.18 at http://www.projectcensored.org. Wonder if it will make the media in 2009. The stories for 2009 are submitted in 2008 and this story hasn’t been brought MSM… I submitted Judd’s piece with the first discovery in it today. It has been a week since he published it, and nobody has picked up on it. Madoff scandal took over.

There is an interesting article for 2009 no. 24 about media censorship… American journalist in Japan…UPDATE BY BENJAMIN FULFORD

“If you still believe that the English language corporate media is free, take a look behind the scenes at the Foreign Correspondents Club of Japan (FCCJ) and think again.

I was a member of that club for over two decades, but I had no clue about what it really represented until I tried to stage a press conference about 9/11. From that point on all sorts of nasty things started to happen and I suddenly realized the place seemed more like a nest of spies than a club for journalists.

For example, people I did not know tried to have me evicted from the club, e-mails vanished from my inbox before I got to read them, and people started to spread the word that I had mental issues.

The list of insults to press freedom at the club since that initial conference is too long to write about in detail here, so I will merely cite the most recent example. ”

http://www.projectcensored.org/top-stories/articles/24-japan-questions-9-11-and-the-global-war-on-terror/

Here may be one that gave Madoff trouble and maybe still giving others the same.Check from about three months back.

Do I hear JPM squeeling like a pig?

Detailed Quote – ROYAL GOLD INC – http://www.royalgold.com

Sym-X Bid – Ask Last Chg % Vol $Vol #Trade Open-Hi-Lo Year Hi-Lo Last Trade News Delay

RGLD – Q no orders 48.43 +1.70 3.6 338.3 15,710 2,010 47.11 48.91 46.27 47.31 22.75 Dec 26 16:13:03 Nov 05 15 min RT 1.5¢

Trade times are ET. News times are ET. Bid/ask/vol sizes in thousands.

Nasdaq Indicators — Market: Nasdaq — Bid Tick: Down — UPC Restricted: No

Pink Sheets Indicators — Primary Market: Nasdaq — Tier: None — Status: Active

Fundamentals · Holders · Forum · Trade Workstation · Market Depth · 3 Month Closes · Technical Charts – 1 Yr | 3 Yr | 5 Yr | 10 Yr · Java Charts – Intraday | Historical · · 1yr Bulletins · Historical · Options · Portfolio

Recent Bulletins

There are no recent headlines for this symbol.

Recent Trades – Last 10

Time Ex Price Change Volume

16:13:03 Q 47.6889 +0.9589 100

16:13:02 Q 47.6889 +0.9589 100

16:12:54 Q 47.6889 +0.9589 300

16:12:53 Q 47.6889 +0.9589 100

16:00:22 Q 47.8016 +1.0716 3,400

16:00:04 Q 48.43 +1.70 209

16:00:01 Q 48.43 +1.70 5,662

15:59:57 Q 48.49 +1.76 100

15:59:56 Q 48.49 +1.76 100

15:59:53 Q 48.49 +1.76 100

1 Year Chart for rgld Just the Image For Printing

3 Months Close Prices

Date Ex : Sym Open High Low Close Chg Vol #Tr Bid Ask

2008-12-26 Q : RGLD 47.11 48.91 46.27 48.43 1.70 338,308 2010

2008-12-24 Q : RGLD 46.78 47.258 45.5701 46.73 -0.05 221,242 1424

2008-12-23 Q : RGLD 45.678 47.31 45.02 46.78 1.77 762,962 4843

2008-12-22 Q : RGLD 45.99 46.84 44.01 45.01 0.22 867,633 5268 44.32 45.51

2008-12-19 Q : RGLD 43.134 45.00 41.00 44.79 2.77 1,566,495 5249

2008-12-18 Q : RGLD 43.65 44.25 41.34 42.02 -1.56 1,082,178 7298 41.36 43.85

2008-12-17 Q : RGLD 43.67 46.68 43.54 43.58 0.19 1,628,701 9253

2008-12-16 Q : RGLD 40.36 43.54 39.45 43.39 3.78 1,051,032 6112

2008-12-15 Q : RGLD 39.03 41.37 38.83 39.61 0.78 831,257 4788 39.01 40.10

2008-12-12 Q : RGLD 36.50 39.39 36.41 38.83 1.77 480,351 2926

2008-12-11 Q : RGLD 39.24 40.95 36.59 37.06 -1.56 868,011 5161

2008-12-10 Q : RGLD 37.50 39.01 36.61 38.62 2.33 564,724 3244

2008-12-09 Q : RGLD 35.96 37.66 35.60 36.29 -0.57 672,454 4969

2008-12-08 Q : RGLD 38.9999 39.77 36.15 36.86 -0.33 813,844 4883

2008-12-05 Q : RGLD 36.00 37.33 34.31 37.19 0.24 638,807 4111

2008-12-04 Q : RGLD 37.48 39.14 36.38 36.95 -0.58 621,394 3969

2008-12-03 Q : RGLD 37.00 38.50 36.34 37.53 -0.34 712,981 5078

2008-12-02 Q : RGLD 35.13 38.12 34.93 37.87 3.03 823,973 5249

2008-12-01 Q : RGLD 37.43 38.99 34.79 34.84 -5.16 882,137 5342

2008-11-28 Q : RGLD 38.07 40.00 37.39 40.00 0.53 353,522 2246

2008-11-26 Q : RGLD 38.44 39.99 38.00 39.47 0.56 530,712 3459

2008-11-25 Q : RGLD 38.27 38.93 36.72 38.91 0.82 694,054 4476

2008-11-24 Q : RGLD 35.84 38.97 35.10 38.09 3.36 1,470,485 8374

2008-11-21 Q : RGLD 31.07 34.95 30.78 34.73 5.06 1,249,040 8028

2008-11-20 Q : RGLD 30.92 31.87 29.50 29.67 -0.71 622,675 4079

2008-11-19 Q : RGLD 30.47 32.24 30.34 30.38 0.05 897,821 5003

2008-11-18 Q : RGLD 30.712 30.83 29.51 30.33 0.18 683,172 4630 29.70 30.98

2008-11-17 Q : RGLD 30.60 31.80 29.48 30.15 -0.73 505,405 3342

2008-11-14 Q : RGLD 31.86 32.98 30.55 30.88 -1.13 637,350 4182

2008-11-13 Q : RGLD 28.98 32.16 27.23 32.01 3.20 729,462 4750

2008-11-12 Q : RGLD 31.33 31.50 28.80 28.81 -2.76 582,003 4130

2008-11-11 Q : RGLD 30.45 32.54 30.07 31.57 0.10 559,299 3959

2008-11-10 Q : RGLD 31.72 32.33 30.53 31.47 0.98 427,202 2987

2008-11-07 Q : RGLD 29.20 31.39 29.20 30.49 1.25 502,420 3345

2008-11-06 Q : RGLD 31.60 32.20 29.20 29.24 -1.72 590,979 3439 45.99

2008-11-05 Q : RGLD 30.17 32.09 29.61 30.96 0.44 730,236 3937 31.08

2008-11-04 Q : RGLD 29.02 30.78 29.02 30.52 1.81 764,727 4764

2008-11-03 Q : RGLD 28.01 29.93 28.01 28.71 -0.12 486,803 3529 30.25

2008-10-31 Q : RGLD 27.72 29.90 27.53 28.83 -0.20 483,129 2845 30.45

2008-10-30 Q : RGLD 28.54 29.49 27.09 29.03 1.34 522,486 2806

2008-10-29 Q : RGLD 26.00 28.56 25.67 27.69 2.15 804,405 4260 27.27 28.64

2008-10-28 Q : RGLD 23.78 25.64 23.29 25.54 2.39 803,990 4431 23.97 24.03

2008-10-27 Q : RGLD 24.22 25.45 23.06 23.15 -1.69 711,802 3576 25.50

2008-10-24 Q : RGLD 24.51 26.23 22.75 24.84 -0.20 1,065,350 6054 23.93 25.87

2008-10-23 Q : RGLD 25.08 28.12 24.03 25.04 -0.67 1,238,505 6019 25.11 25.73

2008-10-22 Q : RGLD 28.39 28.39 25.60 25.71 -3.18 1,168,294 6639

2008-10-21 Q : RGLD 30.50 30.64 28.85 28.89 -2.58 655,758 4058

2008-10-20 Q : RGLD 29.53 31.67 28.76 31.47 2.47 684,925 3691 27.00 36.00

2008-10-17 Q : RGLD 30.64 31.30 28.88 29.00 -2.23 1,231,120 6215

2008-10-16 Q : RGLD 33.46 34.26 29.20 31.23 -2.33 1,450,381 7319

2008-10-15 Q : RGLD 36.52 37.59 33.12 33.56 -3.44 693,987 3665

2008-10-14 Q : RGLD 36.82 37.76 35.17 37.00 0.33 1,092,936 6263

2008-10-13 Q : RGLD 37.47 38.38 34.69 36.67 -0.65 812,549 4555

2008-10-10 Q : RGLD 40.75 40.92 34.37 37.32 -2.38 1,427,100 6869 36.09 36.71

2008-10-09 Q : RGLD 38.92 40.32 38.40 39.70 -0.03 1,280,945 6558

2008-10-08 Q : RGLD 34.49 39.95 33.90 39.73 5.48 1,217,981 5619 39.67 40.00

2008-10-07 Q : RGLD 35.98 36.81 34.19 34.25 -0.23 753,605 4448 33.78 34.82

2008-10-06 Q : RGLD 35.80 36.83 32.10 34.48 -0.69 1,209,932 7388 39.85

2008-10-03 Q : RGLD 34.88 37.28 34.01 35.17 0.79 630,059 4025 35.25

2008-10-02 Q : RGLD 37.00 37.17 34.14 34.38 -3.23 826,415 5494

2008-10-01 Q : RGLD 36.23 38.80 35.60 37.61 1.65 772,337 5327

2008-09-30 Q : RGLD 36.52 36.78 35.09 35.96 -0.90 682,165 4740 39.50

2008-09-29 Q : RGLD 36.11 38.29 35.59 36.86 -0.32 650,074 3934 39.85

Sorry the chart for RGLD would not paste and that shows the action in a very visable way.See it here.

http://www.stockwatch.com/swnet/utilit/utilit_snapsh_result.aspx

Pam Martens wrote an article in January about the derivatives market, and exposed who are the owners of Markit, These derivatives are to bonds what options are to stocks. We know how options were used. Naked shares were dumped into the market to make the puts valuable and the OMM could naked short or rent out his exemption.

It follows that the undelivered bonds that were rampant in the market were used to manipulate the derivatives market so that the players could profit. http://www.counterpunch.org/martens01212008.html

She just published another article on the Madoff DC connection. http://www.counterpunch.org/martens12222008.html

Who is the man behind the curtain?

I think Madoff is a front man, the tip of a much bigger iceberg, the guy who facilitated a much bigger crime.

1. All money in the west is privately created.

2. Creation of money requirings borrowing.

3. Since interest is never created, the system is short. That means the money supply has to continuosly increase (inflation) until the inevitable mathematical collapse.

This site theorizes that Madoff and the credit derivatives ponzi scheme were about delaying the inevitable collapse and preserving the banksters’ power.

http://www.conspiracyplanet.com/channel.cfm?channelid=102&contentid=5653&page=2

http://en.wikipedia.org/wiki/Kondratiev_wave

These parasites started as parasites of England and are currently parasites of America, but they have no allegiance to anyone other than a world system they can control.

Dorothy, bringing the NSS problem to wider recognition is problematic, in part because some folks try to associate it with what I regard as lunatic conspiracy theories. Yes, I know some demented souls think that the Illuminati runs the world and that hidden explosives brought down the WTC towers, but then mental illness is as old as mankind.

What we have here with NSS is a very REAL phenomenon with a public relations problem, in part because at a glance it resembles another tinfoil hat conspiracy theory. Just look at all the derision Patrick has bravely withstood over the past three years while bringing it to light. Efforts to rope stock counterfeiting in with grassy knoll type theories are, in my view, at best misguided and at worst attempted sabotage.

Patrick

Madoff : chock full of NSS? Its a racing certainty.

PT

On Feb 25th, 2006, Joe Nocera wrote in “Overstock’s Campaign of Menace”, referring to Rocker/Copper River, “Now, however, the firm has instituted a policy of not talking to the news media.” http://query.nytimes.com/gst/fullpage.html?res=9C00E7D91F3EF936A15751C0A9609C8B63&sec=&spon=&pagewanted=2

This apparently this policy didn’t apply to e-mails because Cohodes corresponded with Bethany McLean on Dec. 7, 2006. .

Fairfax initiated their lawsuit on July 26, 2006 and even that didn’t stop communication, so it shows that neither public comments or lawsuits has a “chilling” effect Cox was afraid of if subpoenas were issued by the SEC as the parties had to know that subpoenas would be issued for discovery.

re:mhelburn

“I stopped by Wiki and noted that overall, Patrick’s bio has been cleaned up and happened onto http://en.wikipedia.org/wiki/Intercollegiate_Studies_Institute This is an organization that works to stifle discourse as an agenda.”

What’s the point of that lie regarding ISI?

Judd, was looking at some recent data on Morgan Stanley that looks interesting. considering that this is ‘net’ settlement and all it would certainly appear that a bear raid was on WRT Morgan Stanley despite the comment memo’s by the industry who beg to differ.

http://investigatethesec.com/drupal-5.5/?q=node/530

I do have to say, someone impersonating me means I’m putting a dent in their diseased minds. Here’ s the comment, #22, which will be removed soon. Thank you, whomever, for validating my mission.

# lenofus Says:

December 28th, 2008 at 6:45 am

That’s insane. I have re-read this blog and now think you all need to spend more time outdoors.

How do I reconcile the SEC’s claim that fails to deliver and receive combined total only $6 billion, when in 2001 they admitted it was already at $94 billion and climbing rapidly?

http://www.google.com/search?hl=en&q=site%3Ahttp%3A%2F%2Fwww.404.gov%2Fabout%2Fannual_report

1995 SEC Annual Report

Securities Failed to Deliver increased 24.7% from 1993 to 1994, totaling $22 billion. (pg. 147). Revenues from trading against customers went from $15.7 billion in 1990 to $20.2 billion in 1994. Clearing firms made 82% of the securities industries revenue even though they only represent less than 10% of brokerages (pg. 144).

__

The 2007 annual report no longer provides this detail and their only mention of shorting is to say they did a pilot and found they could remove the bid price test without any threat to the capital markets (ya right). They commend Annette Nazareth, who is responsible, personally for regulating shorting and clearing brokerages.

__

According to the 2002 annual report, pg 172, fails to deliver went from $19.2 billion (.7% of assets) in 2000 to $94 billion (3% of assets) in 2001.

http://www.sec.gov/pdf/annrep02/ar02full.pdf

I can’t help but think that the SEC’s decision to stop including this data and the sudden jump in fails coincides nicely with the dot com crash which made someone trillions, the NYSE divestment of liability in their Euronext IPO and the formation of the DTCC.

I finally found the 2007 data in a separate file.

http://www.sec.gov/about/secstats2007.pdf

According to the SEC, fails to deliver increased 69.5% from 26.4 billion in 2005 to 44 billion in 2006. How do I reconcile this with the BS they publish on their SHO page?

Note that this is cash value after the stocks have been punished into oblivion (note everything tanks towards the Dec. 31 disclosure date) and excludes all fails hidden in Canada and Germany and assumes the thieves are providing the SEC with accurate records even though it appears no one ever audits their FOCUS reports.

To put the value of fails in perspective, the industry as a whole only had $81.4 billion in cash in 2006.

All the trading for the entire year of 2006 was $48.2 trillion or approximately $192.8 billion per day. That means the fails we know about equal a little less than 1/3 of the entire value of a typical trading day.

They claim that complaints against short selling fell from 631 in 2006 to 604 in 2007 and that it is only the 8th most common complaint (implying that since reg. SHO, shorting complaints have slowed down).

umm couild it be that the SEC is being less than “honest”?

Transcript of DTCC and other industry arguments against letting beneficial shareholders vote their shares.

http://www.sec.gov/news/openmeetings/2007/openmtg_trans052407.pdf

Interesting, Larry called Cede & Co. “CDINCO” and said the DTC was formed in 1973 and NSCC in 1976 in response to a paperwork crisis in the 1960’s and relying on congressional securities act ammendments from 1975. He compares the DTC to a commercial bank and compares the fractional backing of entitlements with real shares to the fractional backing of bank deposits with real money. In other words, he thinks that the DTC has the right to fractionally back beneficial ownership even though they have a trust agreement to act as a custodian.

Here’s what he thinks of what brokerages should do with your money:

“That obviously adds tremendous liquidity to the 8 program. You don’t have brokers and banks tying up their 9 capital into trades on a trade for trade basis. They can use 10 that capital to invest in other things”

Chevron suggested that the SEC was set up to protect retail brokerage rights and the whole OBO concept is ridiculous. Why wouldn’t you register the names of the actual beneficial owners of the property?

Then the brokerage comments. They send out the number of proxy cards that equal the number of entitlement holders, then hope some of them don’t return the cards. The ones that return the cards are allocated available votes, pro rata. In other words, if 200% of the cards come back, you get .5 of a vote instead of the full vote a certificate holder would get. They talk about “pre-balancing” and “post-balancing”.

The next quote should make you mad:

“That obviously adds tremendous liquidity to the 8 program. You don’t have brokers and banks tying up their 9 capital into trades on a trade for trade basis. They can use 10 that capital to invest in other things”

On average, 31 out of 288 clearing brokerages tried to vote more shares than they actually had. I would suggest the other ones were smart enough not to try to vote the extra entitlements. SIFMA set up a prevention system to make sure clearing brokerages tuned down their voting to match what they actually had at the DTC.

– Other markets register beneficial owners names.

– institutions can borrow stock to vote it, without short selling it. (Keep the borrowed stock long in their account). Osama Bin Laden could borrow stock and be the largest controlling voter, without actually owning anything.

– professor “OTC derivatives revolution in particular has undermined the integrity of and

the transparency of this finely wrought system.”

– “our goal is not to have the perfect coupling of shares and economic interests…interfering with the share lending market, which is essential to short sellers and the proper pricing of shares.”

Transcript of SHO rule making, Sept. 15 2006

http://www.sec.gov/about/economic/shopilottrans091506.pdf

The word “grandfather” didn’t come up once, nor did the phrase “comment letter”. 100% of the people speaking supported naked shorting.

“But it seems to me that the optimal thing for the market maker to do might be instead of holding a large inventory when somebody comes with a buy to sell to them, you know, if somebody comes to the buy, just short it, just borrow it. It lowers your inventory cost.”

(SEC study)

“First of all, it was rather surprising to see how large a percentage of sell orders are short sell orders. As you can see there’s roughly 23 percent of all sell orders are short sell orders, a surprisingly large percentage.”

“We also found out that short sell orders were much more likely to be canceled or to simply go unfilled and expire than regular sell orders. The reason for that is because of the uptick rule.”

– there are usually more buys than sells when you look at market depth. Unless the price rises unnaturally, the only way to match it is to increase ask depth by 30% (naked shorting)

– allowing prices to rise by reducing shorting will lower average investment returns

– a higher price encourages companies to raise money and then waste it

– “If you look at the history of enforcement actions at the SEC, the number of actions to deal with pump and dumps vastly, vastly exceeds the number associated with bear raids. Bear raids are very uncommon.”

– shorting protects investors from paying too much “How many traders complained about being sold very high priced stocks in the late 1990s, and then after that lost a lot of money? I think huge numbers of small investors felt in retrospect like they got ripped off.”

– “So I agree with Larry that the short sellers are the big ally of the SEC in its efforts to protect small investors from schemes that would, essentially, be manipulative.”

– “the locate rule is an effort to throw a little bit of sand into the gears that would otherwise smoothly allow a market for borrowing and lending securities to operate.”

– And one of the proposals that I understand is up for discussion is whether buy-ins should be more strictly enforced to eliminate short positions on which traders have failed.

If you more aggressively force traders to liquidate their short positions, you make it easier for someone to corner the market and squeeze the shorts in the stock market. This would have the bad effect of making the schemes that Larry talked about, the pump and dump schemes, easier to execute and would, I think, therefore, be kind of a bad idea. So rather than have a forced buy-in for short positions that have been failed on for a long period of time I would recommend as an alternative just a series of escalating modest penalties”

– the cost of naked shorting falls to zero when interest rates are at zero as the only cost is borrowing to cover the margin on the fail

– “Short sellers are very important parts of our capital markets. Short sellers get pessimistic information into prices. We don’t want just the optimists to have a vote. We want to have pessimists also to express their view.”

– “I would characterize short sellers as an oppressed minority.”

– “why we were worried about downward price manipulation but were not worried about upward price manipulation. So it seems an odd, sort of, asymmetrical rule.”

– “I think banning trade, which is, essentially, what the uptick rule does, is rarely a good idea”

– “I was getting progressively more sad and more sad going through this discussion here. And I kept thinking poor uptick rule. I mean, it has been with us for 70 years now. Anybody to stand up in defense of the uptick rule? Well, it’s not going to be me. Of course, the other challenge I have I’m the last here, and so how can I make it different and interesting.”

– “short sellers are already handicapped, a lot of restrictions.”

– the retail investor “facing the lions and debating whether the ethics of eating someone that’s there to be eaten.”

– “the smallest stocks right now aren’t subject to the tick test, and you don’t see a lot of people clamoring for it. Of course, those are the ones that are most subject to the pump and dump.”

– the commissioners get spam emails telling them to buy stock, but they can’t go after the spammers at they have a right to express their opinion from eastern Europe. Naked shorting needs to be allowed to protect unsophisticated investors from paying too much for these scams.

– retail investors are often confused

– “But if they were going to be threatened with a buy-in on their 100 percent of the flow, that would eliminate their ability to protect the small investors from exorbitant prices.”

– “What I’m worried about is, you know, you publish stock ABC. It has a lot of short interest, and the CEO of stock ABC, who is a evil pump and dump guy, sees that and uses that information to somehow manipulate the securities lending market.”

– “Ken Lay’s defense was that Enron was a victim of a bear raid. I didn’t buy it. The jury didn’t buy it. I don’t know if anybody bought it. But the bear raid is the story that a CEO tells when the market is voting against him.”

– “I think bear raids probably occur hardly ever”

– “who is going to complain about being able to buy depressed stocks at really cheap prices and earning a great return on that?”

– “So after September 11th there was a massive manhunt for the alleged — Osama bin Laden was allegedly short selling airline stocks on September 10th. So there was quite a search for nefarious short sellers after that,”

– “The example of Osama bin Laden is insider trading, not a bear raid. Let’s make sure we have the distinction right.”

– “Maybe we should have transparency where everybody’s Social Security number is posted on the internet. That would be a form of transparency most of us probably wouldn’t like.”

david n.-to compound your numbers you must realize that the NSCC failures to deliver that are “pre-netted” out of existence by the NSCC’s CNS system aren’t tallied nor are those held where the “trade comparison” was done in an ex-clearing format. Here’s a snip-it from a paper I did recently on NSCC “pre-netting” and how it obfuscates the severity of our abusive naked short selling issues.

I think it wise to digress for a moment and address some of the idiosyncrasies about “netting” as it relates to our DTCC-administered clearance and settlement system. “Netting” is a wonderful streamliner in a business as overwhelming as processing the trades done on Wall Street is but it has some limitations. If one is going to reap the rewards of the enhanced efficiencies and streamlining of processes in our clearance and settlement system associated with “netting” one has to realize that the system is based on the presumption that all DTCC “participants” and their hedge fund “guests” are going to “act in good faith” with their superior knowledge of, access to and visibility of the playing field on Wall Street. If they don’t then all bets are off as to realizing those enhanced efficiencies without greatly diminishing the integrity of the overall clearance and settlement system. This has to do with how the DTCC operates. As we just reviewed the 4 ways to effect “trade comparison” are CNS, non-CNS, trade for trade and ex-clearing.

Let’s assume that on a certain day a buying market maker “B” has a client that purchases 100 shares of “Acme” from selling market maker “S” in the morning. Let’s also assume that “S” receives a buy order in the afternoon from a client for 100 shares of Acme which it buys from market maker “B”. Let’s further assume that both MMs naked short sold into the orders while theoretically acting as a bona fide MM and that both orders resulted in failures to deliver at the NSCC. In the NSCC’s “Continuous net settlement” (CNS) system there will be no necessary net transfers of securities of Acme at the end of the day between the 2 MMs even though there are 2 FTDs generated which leads to the procreation of 200 readily sellable “securities entitlements”. The share price of Acme Corporation will be pressured downwards by this extra “supply” of readily sellable “securities entitlements” because they are freely tradeable as if they were legitimate shares of Acme which they are not. Note the “Disconnect” involving “netting” having nothing to do with the delivery status of that which is being “netted”. They are two independent variables. Note also that “good form delivery” is needed for a securities transaction to legally “settle” and that Section 17 A of the ’34 Exchange Act mandates that all securities transactions must “promptly settle”.

At the NSCC this trade involving 2 FTDs but no net transfer of securities necessary (via “balance orders” in non-CNS settlement) at the end of the day still got filed into the “trade settled” category from a CNS point of view even though it didn’t “settle”. At the broker/dealer level things look wonderful in regards to this transaction but at the client level 2 investors did not get that which they purchased. This is not to say that an FTD and an FTR (fail to receive) were not generated because they were but they’re held on the books of the 2 MMs and not at the NSCC in its CNS system. A full 97% of transactions are “netted” via the NSCC.

The NSCC wants nothing to do with the contents of the books of its “participants” and what they “imply” on their monthly brokerage statements that they are “holding long” for their clients. Both “bilateral” and “multilateral” continuous netting can provide a wonderful cover up to fraudulent activity. Any theoretically unconflicted SROs (like the DTCC) that use “netting” and especially “continuous netting” would obviously have meticulously designed controls in place to detect and address delivery failure related abuses (DFRAs). The obvious control measure of choice would be to buy-in any delivery failures that last longer than the maximum age of a legitimate delivery failure yet this SRO, the NSCC, pleads “powerless” to effect buy-ins of their abusive “participants” that refuse to deliver that which they sell. Why not? Because it’s not in the financial interests of their abusive “participants” and the unregulated hedge funds that dispense $11.2 billion annually to the DTCC “participants” willing to be the most “accommodative” to the financial interests of the hedge fund manager.

Even though the DTCC acts as an SRO (“Self-Regulatory Organization”) mandated to create and enforce rules and regulations associated with the “business conduct of its participants” they don’t particularly care if their “participants” that have 10 million shares of an issuer in its “participant’s share account” at the DTCC implies to its clients that it is holding 18 million shares “long” somewhere. One might think that that would be a good “control” procedure for an SRO that administers a clearance and settlement system as easy to defraud as one based on “continuous net settlement” wherein the delivery status of shares sold is obfuscated.

In the DTCC-administered clearance and settlement system there are various vantage points that must be kept in mind. The CNS status of what is owed between 2 “participants” at the end of a trading day is but one vantage point. The securities contained in the “participants’ NSCC shares account” is another one as is the amount of paper-certificated shares held in the DTC subdivision’s vault system. The positions held within the b/d away from the NSCC is another one as is what the b/d “implies” on its monthly brokerage statements as the “securities being held long” on behalf of the client are.

The reality is that a securities transaction at the NSCC that was “successfully netted” has nothing to do with “good form delivery” and therefore “settlement” of the trade having been achieved. Imagine how misleading the level of the “FTDs” reported from the NSCC in regards to the Reg SHO “threshold lists” are when delivery failures aren’t necessarily “delivery failures”.

According to the SEC, failures to Deliver jumped 69.5% from 2005 to 2006, then another 34.6% from 2006 to 2007.

(a) Securities Failed to Deliver 44,726.5 0.8% 60,181.3 1.0 34.6

The current fails are at least $60.2 billion. I believe this is based on NYSE fails (FOCUS reports), which excludes OTC and Pink stocks and any trading hidden outside of America or netted x-clearing between partners in crime.

http://www.sec.gov/about/secstats2008.pdf

Dr. DeCosta, what’s even worse is they can net stock as a fungible mass using repo agreements. I can owe you $1 million worth of Apple and you owe me $1 million worth of crapco and they net to zero.

Both the seller is long, because he agreed to repurchase (a call option) and the buyer is long, because he is the current owner.

Regarding all of the collapses with the brokerages, a number of banks are still extremely vulnerable to the credit crisis.

A list of banks and whether they are in trouble or not. A rating of 50 or higher is bad and over 100, means they will probably fail. If you have money with one, you should move it.

http://www.lewrockwell.com/chris/banks/banks.html