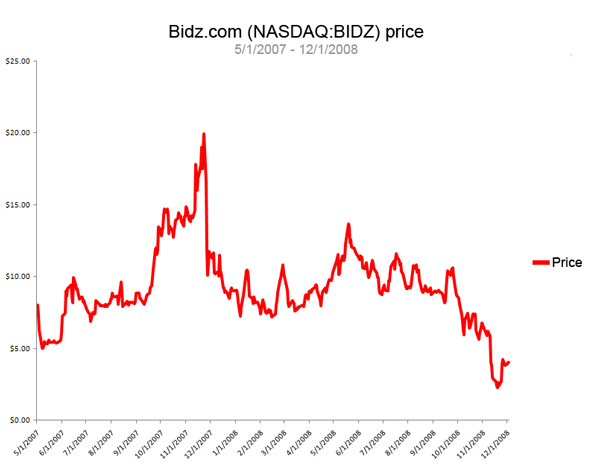

Bidz.com is an online auction company which went public in May of 2007. Take a look at the company’s relatively short price history, to see if you can spot the abrupt 49% drop.

(If you chose November 23-28, 2007 you win the Deep Capture home game!)

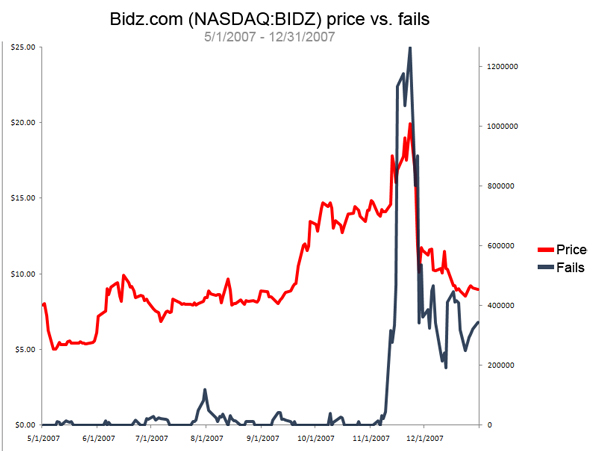

To better understand what was going on during those four trading days, let’s zoom in to look at just Bidz.com’s first seven months, and include each day’s failed trades.

As any regular readers of this blog might have predicted, that 49% drop was accompanied by a similarly anomalous jump in BIDZ settlement failures to deliver (FTDs).

Indeed, during its first 136 days of trading, BIDZ, with a float of under 12-million shares, experienced about 1.5-million FTDs, an average of about 11,000 per day.

Then, in the nine trading days between November 12-23, 2007, nearly 7.2-million shares — averaging nearly 800,000 per day — failed to settle, resulting in a tremendous, artificial swelling of supply of BIDZ shares.

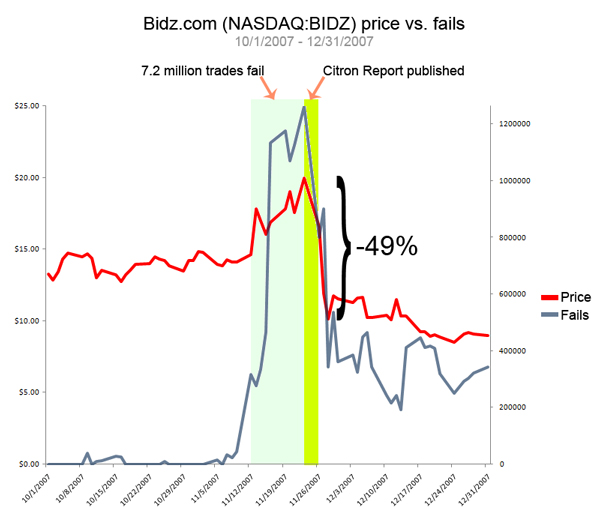

To better understand what happened next, let’s take a closer look at that spike in fails and drop in price, in relation to a particular external event.

November 26, 2007 (highlighted in yellow) marks the date of publication of an attack on BIDZ by short selling blogger Andrew Left of Citron Research (formerly known as “Stock Lemon”). The report made a few subjective observations relating to BIDZ’s inventory levels, as well as revealing the criminal record of one of the company’s vendors: neither of which were good news, but hardly bad enough to justify cutting its share price in half.

This episode is instructive on two levels.

First, it offers insights into how the criminals engaged in the kind of manipulative short selling observed here use other — often engineered — events as “cover” for their activities.

Second, it provides conclusive proof that either Andrew Left’s Citron Reports is a tool of these illegal naked short selling hedge funds, or those hedge funds have clairvoyants on staff.

Given how poorly things have gone for these folks now that illegal naked short selling has grown increasingly difficult to engage in, I’m leaning toward the former.

If this article concerns you, and you wish to help, then:

1) email it to a dozen friends;

2) go here for additional suggestions: “So You Say You Want a Revolution?“

Apparantly there are others that are paying serious attention to Deepcaptures’ blogs and info.

Watch in amazement people!!!

http://www.youtube.com/watch?v=NbaHBGS4fxY

Judd,

Well written blogpost. I like how you go through the scheme step by step.

Perhaps you could incorporate some sort of webapp on DeepCapture that has a list of all the available data on manipulated stock, the share price, *and* the negative reports on the time-axis of that data. That would be pretty compelling proof – to show hundreds and hundreds of companies’ stocks manipulated in this manner.

Oh wait, someone already made a webapp like that:

http://failurestodeliver.com/

Unfortunately this site doesn’t have the negative reports/rumors data on the time-axis.

Keep up the great work!

Well done, Judd.

As an original BIDZ investor (back in the venture stage), I know the story all to well. Note that BIDZ has no debt and has been consistently profitable since before going public. They have consistently met guidance. Their business does not depend on their stock price. Many other companies have problems that the criminal manipulators can pint to as the reason for the stock prive decline. But not BIDZ. No valid criticism of the company has stuck for long.

Mr. Byrne,

Thank you so much for your tireless efforts.

Could you provide a similar analysis for MBIA (NYSE: MBI) and Ambac (NYSE: ABK) from September, 2007 to date? They have been a target of William Ackman for several years and last year was aided by the assistance of Jim Chanos, Whitney Tilson, and other miscreants.

keep up the great work,, I emailed 50 reporters and everyone at company the story,, Build an ARMY company by company their shareholders will all join the fight, Show them how easy it was to loot their money and lets expose those who did it

I have been involved with Bidz since prior to the Citron article. I have paper losses in the area of 100k. I attribute my misfortune to the naked short activity which was aided and assisted by Citron and others. It is a shame the toothless paper tiger (the SEC), doesn’t have the desire or ability to reign in the illegal activity of the hedge funds that share in the responsibility for this naked short activity and losses suffered by the investing public. I intend to to cut and paste this blog to an SEC complaint form and send it in. I know, it is probably a waste of my time……

NAME AND ADDRESS PLEASE. It is the only thing we need to know now. Maybe we can take signs and protest outside the crooks homes.

“Always follow the money Trail” they say. Well, Try looking at Liechtenstein Bank. OH wait, we know there are 19,000 US accounts there as of July 2008, and the list has been turned over, but what, NO PERPS YET ???? Fox gurading the hen house….

I encourage everyone reading this to go to Obama’s web site http://change.gov/page/content/openforquestions

and put your questions regarding this issue in the que. So far, when I do a search of the questions submitted, mine is the only one asking about illegal naked short sales.

This is an educational aid that I have found to be useful in explaining these sometimes difficult to understand crimes associated with “abusive naked short selling”.

FIGURE 1

THE “SELF-LEVERAGING CYCLE OF CORRUPTION AND FACILITATION”

“PRIMING THE PUMP”

An unregulated hedge fund manager takes the funds he receives from wealthy investors as well as borrowed funds from his “prime broker” (“outside” leverage source #1) and places a “short sale” order through one of his “executing b/ds”.

INTRA-CYCLE STEPS

A) The “executing b/d” executes the short sale order (or intentionally mislabeled “long sell” order) and knowingly fails to make delivery on T+3. Note that a bogus “pre-borrow”, a bogus “locate” or claiming a bogus “customer assurance” might be involved. With the relationships involving hedge funds, prime brokers and executing brokers there is always plenty of plausible deniability available as one can always say “but I thought that “X” was taking care of the pre-borrow or locate” or “my client told me that he took care of the pre-borrow or locate and therefore I technically had a “customer assurance” qualifying as a locate.”

B) The resultant “failure to deliver” FTD needs to be “collateralized”. The cash value of the sale plus usually about 2% of the sale value serves as the collateral. The interest earned by this collateral during the life of the delivery failure goes not to the investor who didn’t get what he paid for and whose money it is but is shared by the investor’s b/d and the party failing to deliver according to a formula dependent on how expensive a legitimate borrow would have been had it been done i.e. “hard to borrow” securities versus “easy to borrow” securities and “rebate spreads”. This is independent of the fact that a legitimate borrow never did occur.

C) The FTD results in the issuance of readily sellable (dilution causing) “securities entitlements” which accumulate in the share structure of the corporation previously targeted for attack.

D) This extra “supply” of readily sellable “entities” (legitimate shares plus mere “securities entitlements”) predictably causes the share price to drop. The laws of supply and demand still interact to determine share price through the “price discovery” process it’s just that the individual variables of “supply” and “demand” are subject to manipulation.

E) As the PPS drops the “collateralization” requirements lessen and the investor’s money is shunted to the abusive naked short seller despite his refusal to deliver that which he sold; after all it doesn’t exist. This money can then be taken outside of the cycle (dotted lines labeled “self-leveraging #1”) and reintroduced into the cycle at step “A” and be used to assume and collateralize that much higher of a naked short position. This added “self-leverage” or “self-generated leverage” (the money stolen from the unknowing investor) created out of thin air increases with each trip around the cycle as the share price predictably drops. This is over and above the continued day to day naked short selling needing to be done to keep the collateralization requirements manageable for naked short positions that have “accidentally” become astronomical because the targeted company refuses to die on cue.

F) If the corporation under attack is not yet cash flow positive then it is forced by necessity to pay its monthly burn rate by selling an excessive amount of “legitimate” shares at an artificially depressed level (via “manipulation”) to raise a fixed amount of money. This “forced dilution” for yet to be cash flow positive corporations involves legitimate shares and not the mere “securities entitlements” associated with failures to deliver (FTDs) which are synonymous with refusals to deliver (RTDs).

G) These “extra” legitimate shares further depress the PPS.

H) This results in another lessening of the “collateralization” requirements for those refusing to deliver that which they previously sold and yet more of the investor’s money is shunted to the seller of nonexistent shares again despite his refusal to deliver that which he sold as the DTCC has previously illegally converted the clearance and settlement system in the U.S. from “good form delivery” versus payment (DVP) to mere “collateralization versus payment” (CVP).

I) These proceeds can also be taken out of the cycle (dotted lines labeled “self-leveraging #2”) and reintroduced back into the cycle at step “A” to assume and collateralize yet another wave of naked short selling. The result is the self-fulfilling prophecy that this corporation is going down.

OUTSIDE OF THE CYCLE

1) Wealthy hedge fund investors place money into the hands of hedge fund managers. They pay a usurious rate of 2% of funds under management and 20% of all profits (or more) to their hedge fund manager. Why would the wealthy pay these exorbitant rates when the minimum investment is often $1 million? Don’t you usually get a “volume discount” when you invest larger amounts of money? The reason is that this is the cost of admission for being granted access to the “self-leveraging cycle of corruption and facilitation” which they otherwise couldn’t access. In most unregulated hedge funds the cost of admission to access the “cycle” is $1 million minimum plus the “2 and 20”.

2) The prime broker of the hedge fund does the back office work involved and also loans cash to allow hedge fund managers to utilize “outside leverage” which is different from but additive to the “self-generated leverage” created within the cycle. With their own money in play the prime broker is now financially motivated to do everything in its power (bend or break as many rules as possible) to make sure that the “bets” placed by hedge fund managers against targeted corporations work out for the best.

3) All throughout the cycle the various “facilitators” of these frauds get a piece of the action (the investor’s lost money) spun out to them in the form of enhanced order flow, commissions, fees, “mark-ups”, clearing fees, etc. The hedge fund managers will naturally seek out the DTCC “participants” willing to be the most “accommodative” to the financial interests of the hedge fund manager. These market intermediaries acting as “facilitators” to these frauds will get their palms “greased” in an effort to lubricate the cycle so that it spins freely so that the targeted corporation can go down that much quicker.

4) The money of the hedge fund clients, the prime brokers and that stolen from unknowing investors with each spin of the cycle serves to “drive” the cycle while the wallets of the investors is clearly the “target” of the cycle. As the cycle spins round and round the share price of the corporation under attack drops lower and lower which serves to attract the funds of new victims sensing opportunities in the resultant bargain basement prices. Any meticulously-designed fraud will provide for the constant inflow of fresh money from new victims as the old victims get fleeced, take their losses before they get any larger and limp off.

5) The hedge fund manager takes his “2 and 20” periodically as per the agreement with his investors. If he is allowed to “mark to market” his paper profits in short positions and periodically cash in on them without covering these “open positions” then with the DTCC policies currently in effect he can avoid ever covering his naked short position which would have the untoward effect of driving up the share price of the targeted corporation in the process which would diminish his profits and increase the collateralization requirements on his yet to be covered naked short position.

6) Let’s go back to the beginning and recall how DTCC policies render this IOU known as a “securities entitlement” that resulted from an FTD basically equivalent to an unbinding pledge to “eventually” deliver that which was sold unless of course the corporation under attack goes bankrupt in the meantime. This “pledge” buys enough time for these securities fraudsters to fire up the “cycle of corruption” and get it hitting on all 8 cylinders.

7) An analogy that comes to mind involves the type of firework known as a “pinwheel”. You nail it to a fence post and light its fuse and it will spin round and round while showering sparks all over the place. The sparks flying represents the money of those shareholders that bought both fake shares from the securities fraudsters as well as real shares from legitimate sellers of shares that is showered upon all of the “facilitators” to these frauds as well as those pulling the trigger on the actual naked short sales. After the “cycle of corruption” spins for a while then the firework comes to a rest and just smolders for a while like the remains of the corporation that just got torched.

ANALYSIS

First of all this “cycle” described is the bare bones version of reality simplified for educational purposes. My full blown model is much larger and it identifies the existence of many, many entry points into the same basic cycle. This simplified model does not even address ex-clearing arrangements, the role of the ECNs, “sponsored direct access programs”, service bureaus, abusive MMs illegally accessing the exemption from making pre-borrows or locates, etc.

Hopefully even the ridiculously simplified version can reveal to those in authority why the previous measures of the SEC proved to be woefully deficient. What are the salient components of the simplified version of the model: 1) Unregulated hedge funds operating in the dark. 2) The option to refuse to deliver that which you sell. 3) The necessity to merely collateralize the resulting debt i.e. “collateralization versus payment” (CVP) as opposed to “delivery versus payment” (DVP) as recommended by the Bank for International Settlements (BIS) and IOSCO’s Technical Committee on Payment and Settlement Systems. 4) The unconscionable allowance of those absolutely refusing to deliver that which they sold to gain access to the funds of the investor being hoodwinked. 5) The resultant access to the “Self-leveraging cycle of corruption and facilitation”.

The realities of meaningful reform literally jump off the page at you. YOU CAN’T ALLOW FAILURES TO DELIVER TO EVEN OCCUR IN ANY WAY, SHAPE OR FORM IN A CLEARANCE AND SETTLEMENT SYSTEM ILLEGALLY CONVERTED INTO A “CLEARANCE AND COLLATERALIZATION” SYSTEM BECAUSE OF THE RESULTANT ABILITY TO ACCESS THE “SELF-LEVERAGING CYCLE OF CORRUPTION AND FACILITATION”.

Hence this brings us back 54 pages in this document to the aforementioned need for “Hard decrementing pre-borrows” (HDPBs) and “Hard delivery requirements” on T+3 with no exceptions except in the case of truly bona fide MMs willing to prove their bona fides by placing a like-sized bid simultaneous with any naked short sale at 98% of the level he is naked short selling at. In other words a theoretically bona fide MM must prove in advance that he is legally accessing that powerful but universally abused exemption from “pre-borrows” and “locates” accorded only to bona fide MMs while acting in that capacity. Like former SEC Chairman Donaldson clearly articulated when asked how much of this theoretical injection of liquidity by short sellers done for purely fraudulent purposes should he put up with. His answer was a resounding “None”!

For all parties excepting truly bona fide MMs you can’t make the sale UNTIL that which is being sold is already in place to be delivered on T+3; no more extension of “credit” and IOUs. The criminals in this arena imply to the purchasers of what they are selling that any delivery failure they are associated with will be of an ultra short term lifespan. Fine, if that’s the truth then let’s just wait that ultra short term period of time NOW until you are allowed to sell that which you are selling. If you weren’t lying about the ultra short termed nature of your delivery failure then it would be no big deal but nobody has the right to poison the share structure of a corporation with readily sellable “securities entitlements” in a clearance and settlement system illegally based upon CVP. This theoretical need for “liquidity” in fast moving markets has resulted in fraudsters literally drowning corporations that they have pre-targeted for destruction with a tsunami of “liquidity”. Again, study the graphs at deepcapture.com clearly showing the share prices of targeted corporations literally being forced off of a cliff as the number of FTDs go ballistic.

This is big folks.

For those with experience in the industry, one of the things traders or hedge funds fear the most is being exposed in a suit of a major market maker . . . we have our wish.

http://www.bloomberg.com/apps/news?pid=20601087&sid=advES8XRiXZY&refer=home

Top article text:

Dec. 11 (Bloomberg) — Bernard Madoff, president of market- maker Bernard Madoff Investment Securities and a former chairman of the Nasdaq Stock Market, was charged by U.S. prosecutors in a $50 billion securities fraud at his investment advisory business.

Madoff, 70, was arrested today at 8:30 a.m. by the FBI and appeared this afternoon before U.S. Magistrate Judge Douglas Eaton in Manhattan federal court. Charged with a single count of securities fraud, he is to be released tonight on $10 million bond guaranteed by his wife and two others, Eaton said. Madoff’s wife was present in the courtroom.

“He’s one of the pioneers of modern Wall Street,” said James Angel, an associate business professor at Georgetown University in Washington. Madoff’s firm was among the first to automate market-making, in which a dealer continually buys and sells stock. The company was among the largest to offer “payment for order flow,” or paying to handle customer orders. “The exchanges didn’t like the practice and questioned whether customers got the best price,” Angel said.

Madoff’s New York-based firm serves hedge funds, banks and wealthy individuals. It was the 23rd largest market maker on Nasdaq in October, handling a daily average of about 50 million shares a day, exchange data show. The firm specialized in handling orders from online brokers in some of the largest U.S. companies, including General Electric Co. and Citigroup Inc.

I’ve been involved in many of these types of cases and believe me, everybody turns everybody else in when one of these hits.

MADF has made markets in most of the stocks subject to FTDs found on the SHO List.

Line up and take your information requests a step higher. You are about to get your chance as probable cause is about to be sitting on your front doorstep.

AMG

I have been quiet here and on our site as we have been very busy . . . and I cannot speak freely about what we are doing . . . for many reasons.

Rest assured we are making solid progress and will, along with all here, be busting a few perpetrators of the fraud that beset the street over the next quarter.

Stay in touch and best to all for a happy holiday season.

[email protected]

I’ll repeat my comment which is probably really annoying after five years, but:

Snowflakes fall on a mountain side and one by one, they pile up, but it seems like there is no change. The snowflakes are so small against the big mountain.

It’s frustrating to call a congressman or write a letter to the editor and see no change, but your complaints are piling up like those snow flakes.

Every little bit seems like frustratingly little, but like the multiple taps it takes to drive a nail home, you are making a difference and you won’t see it at first.

Don’t give up. Keep sending those snowflakes of change. You may not be the one to get the credit, but you are making the system more an more unstable until change is an imperative.

One day, that very last snowflake, as tiny as it is, lands and causes the whole hillside to come down in an avalanche.

Sean: it may interest you to know that Max Keiser had an article about him on Wikipedia until Mantanmoreland (Gary Weiss) lobbied to have it deleted. That happened in 2007, shortly after Keiser started reporting on naked shorting in the US financial markets.

http://www.nypost.com/seven/12042008/business/ponzi_scheme_at_citi_142511.htm

Sept. 1938

History repeats itself.

http://www.time.com/time/magazine/article/0,9171,760148,00.html

http://www.csmonitor.com/centennial/on-this-day/2008/10/october-29-1929-black-tuesday-the-market-crashes-for-the-third-time-in-october-the-great-depression-brews/

How can Chris COX look at data like this and continue to let the SEC ignore naked short selling and say that the uptick rule is not needed.

This dark period in America will be looked back on in history with disbelief that the SEC let the working class in America get their life savings get swindled as some Hedge Funds makes even more money.

In the 2006 book

Overstocked and Understood I tried to let people know of these dangers but our captured media would not do their part to let people know what was happening.

Brian Villwok

One hypothesis that makes sense to me is that the bankster families are protected no matter how much they counterfeit, because they blackmail politicians.

There’s a pattern, such this article about Blagojevich:

“The Governor of Illinois, Rod Blagojevich, has spoken out and let everyone know that the State of Illinois is not going to do business with the Bank of America until they do their part to keep workers in the Republic Windows and Doors plant working or to at least see that they get their severance and vacation pay.”

16 hours before he was arrested.

Or how Spitzer was stopper from investigating the banksters:

http://www.nytimes.com/2008/11/26/nyregion/26spitzer.html?scp=2

I think these politicians are scumbags, but Kay Griggs makes the claim that the banksters use their money to make sure the people in power ARE scumbags, the very people that can be blackmailed.

http://www.kaygriggstalks.com/

Holy DTC

Madoff wipes out the $Palm Beach Bentleys HaR!

$Phew $50b __hiding? you betcha

Dear Mr. Judd Bagley:

Thank you for letting the entire world know what has happened to Bidz.com. This company was brutally-victimized by the Naked Short Selling Criminals — but, it is still standing.

We must never — never give up the FIGHT for justice. It is a monumental, historic task – but, the forces of good in this fight including investigative journalists & fighters like yourself, Mr. Mitchell & Dr. Byrne, will help reveal this STEALTH-NUCLEAR FINANCIAL ATTACK on the stability of the settlement and delivery system of securities.

With so much at stake, and the timeliness of the extreme-need to solve the unrestrained problem of Naked Short Selling, I sincerely hope that all those whose eyes have seen your article about Bidz.com, revealing the corruption, will do their part in helping stop the criminals. What is their part?

EXPOSURE — Post a link to this article and other Deep Capture articles all over the internet. The entire world of legitimate investors want “justice”. But, even now, many people do not understand why the financial markets are in crisis. So, let’s keep on getting the word out — so people will really know that Naked Short Selling and a flawed settlement & delivery system of securities is at the core of today’s financial crisis.

Thanks again Mr. Bagley — for an excellent article of investigative journalism!

May we all have “justice” soon. And, when we see reform finally reach the financial system, we will be proud — and know that we ALL helped to EXPOSE & REMOVE the criminal elements among us.

Hang_’em_High

The stock is not the company and the company is not the stock. The stock price does not affect the company and It’s does not matter if the stock price is driven down to even a penny, if the companys business is sound and solid it just makes the stock even a better buy.

This blater about nakes short selling manipulating the stock is nonsense. If you truly are a long term investor you invest in the financials of the company not it’s stock price. Otherwise you are just a speculator just in to make a quick buck, if you complain about the stock price being manipulated you belong to this group.

The guy writing this BLOG must be having trouble with reality. What a freaking moron!. There were less conspiracy theorists for JFK’s assasination. Keep ranting while your stock sucks wind and you restate financials yet again

Well now it’s two years later and your stock is even lower than it was in Dec 2008. If the shorts are so wrong then why hasn’t the stock rebounded?

If the report was “hardly bad enough to justify cutting its share price in half.” then why does the stock keep going down?

fantastic submit, very informative. I ponder why the other experts of this sector

do not realize this. You must proceed your writing.

I’m sure, you have a great readers’ base already!

Hi everybody, here every person is sharing these kinds of knowledge, thus it’s nice to read this blog,

and I used to pay a visit this blog everyday.