By some quirk of human psychology, it remains difficult for a certain segment of the population to accept the “deep capture” thesis – the notion that our nation’s regulatory bodies and parts of our media have been “captured” (at times, outright “corrupted”) by a powerful, moneyed elite. “No way,” we are told. “Maybe in Nigeria. Europe, sure. But to think it happens in America? That’s a conspiracy theory.”

Yeah? Well, read this:

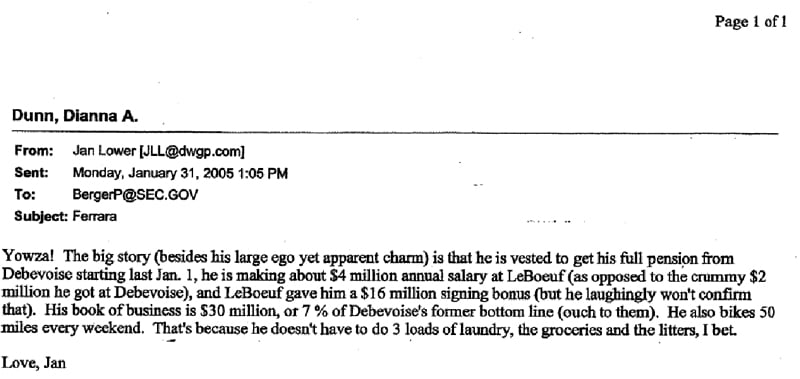

That is an email to Paul Berger, then the associate director of enforcement at the Securities and Exchange Commission. The author, a Washington lawyer, is referring to Ralph Ferrara, a former SEC lawyer who apparently managed to parlay his government service into mansions, maids and millions – by way of a plum position at a law firm called Debevoise & Plimpton.

As you can see, the email was sent in January 2005, soon after the SEC had launched an investigation into alleged naked short selling, insider trading and other misconduct at Pequot Capital, a powerful hedge fund. That same month, the SEC’s lead investigator in the case, Gary Aguirre, was shut out of meetings in which the Commission’s top officials gave Pequot’s lawyers privileged information about the investigation.

By the summer of 2005, some of the SEC’s top officials, including Paul Berger, were maneuvering to have the Pequot investigation whitewashed. When Aguirre tried to interview John Mack, formerly chairman of Pequot and then CEO of Morgan Stanley, he was told to lay off because Mack’s lawyers had “juice” with Berger and SEC Director of Enforcement Linda Thomsen.

Aguirre complained about this in a formal letter to Berger. In response, Berger arranged for Aguirre to be fired – never mind that the SEC had just commended Aguirre for his “unmatched dedication.” At precisely the same time, Berger told Mack’s law firm that he was quite ready to leave public service, and that what he’d really like is to have a job at Mack’s law firm. The name of Mack’s law firm (the law firm with “juice”) was Debevoise & Plimpton – i.e., the same law firm whose multi-million dollar paychecks to former SEC officials had inspired that salivating email.

Perhaps the lawyer who sent that email was merely updating Berger on his colleague’s career trajectory. I have no evidence that the lawyer was trying to influence Berger or the SEC. But the email is a good example of the kinds of conversations that occur with disturbing regularity at our nation’s market regulator. No doubt, those maids and millions were top of mind as the SEC’s associate director of enforcement considered whether he ought to bury an investigation into some serious crimes, fire the whistleblower, and simultaneously apply for a job at the alleged criminal’s law firm.

In the summer of 2006, Aguirre wrote an 18-page letter to the U.S. Congress, blowing this scandal wide open. In this letter, Aguirre noted that his rank-and-file colleagues at the SEC believed that the naked short selling they were investigating had the “potential to seriously injure the financial markets.” So it was all the more appalling when–in November, 2006–the SEC leadership officially closed the investigation into Pequot. In doing so, the SEC said it had found no evidence of insider trading, but it said nothing about the far more serious charges of naked short selling and market manipulation.

Two U.S. Senate Committees spent more than a year looking into this matter. In multiple reports (one more than 700 pages long), Senate investigators did not refer directly to “naked short selling,” but from their descriptions of “market manipulation” and “wash sales” (which are often used to hide naked shorts) it is clear that they believed that Pequot engaged in naked short selling, and that this crime did, indeed, have the potential to “seriously injure the financial markets.”

The Senate concluded that everything about the case – the special treatment received by Pequot and Mack’s lawyers, Aguirre’s dismissal, Berger’s solicitation of Debevoise & Plimpton – was as seedy as can be.

“At worse,” the U.S. Senate stated in one report, “the picture is colored with tones of a possible cover-up.”

Last month – after naked short selling and other hedge fund tricks contributed to the biggest financial cataclysm since 1929 – the SEC inspector general issued a 191-page report confirming just about everything in the U.S. Senate reports. It is impossible to read these reports without concluding that this is the biggest scandal in the history of the SEC–a scandal that entailed a cover-up of precisely those same crimes that “severely injured” (or rather, nearly vaporized) our financial markets.

The SEC leadership responded to the inspector general last week by assigning an SEC employee, who happened to be an administrative judge, but who had no jurisdiction and was not acting in her capacity as a judge, to issue a short document stating that the SEC was innocent – that nobody had acted inappropriately in the case of Aguirre and Pequot Capital. With this document in hand, the SEC announced that it had been “cleared” by “a judge” – making it sound as if there had been some sort of official, independent ruling.

In other words, the corrupt SEC leadership tried to convince us that the corrupt SEC leadership would have the final say on whether the SEC’s leadership was corrupt. The cover-up continued. There was a time when the nation’s journalists would swarm on an abomination such as this. But, alas, there was hardly a peep from our media. Indeed, The Wall Street Journal and other publications helpfully reported that a “judge” had “cleared” the SEC leadership of wrong-doing.

But this scandal is not under the rug yet. And it might grow in magnitude. In a civil case brought by Aguirre, a federal district court ruled earlier this year that the SEC is far from “cleared,” and that it must hand over thousands of internal documents pertaining to the Pequot investigation. The SEC has largely ignored the ruling, turning over documents with much of the relevant stuff blacked out, but it is doubtful that the commission will get away with this. Tomorrow, the court will hold a hearing at which the SEC will likely be ordered to hand over more documents – including those containing evidence of the “market manipulation” (read: “naked short selling”) that helped “seriously injure the financial markets.”

Meanwhile, Paul Berger, the former associate director of enforcement who tried to bury this case, has been made partner at the law firm of Debevoise & Plimpton. I’d tell you how much he’s getting paid for his “juice,” but I hesitate to incite a citizen insurrection.

* * * * * * * *

Mark Mitchell previously worked as a writer for the Wall Street Journal editorial page, chief business correspondent for Time Magazine in Asia, and as the editor responsible for the Columbia Journalism Review’s online critique of business journalism. Send tips to [email protected]

If this article concerns you, and you wish to help, then:

1) email it to a dozen friends;

2) go here for additional suggestions: “So You Say You Want a Revolution?“

$4 million to sellout after the SEC?

Dear Mr. Mark Mitchell:

Thank you for continuing your excellent work at exposing the financial criminals that I refer to as “financial rapists” (Naked Short Sellers).

Although you may not hear it a lot, there are so many people (especially victims of Naked Short Selling) that are so very thankful for what you are doing. I don’t speak for anyone, but I believe every legitimate investor in the world that knows what you are doing — is hoping beyond hope that your investigative journalism to expose these financial criminals — reaps justice.

In a courtroom with a jury of Main-Street-Americans, I certainly hope that the guilty financial criminals will be given the harshest penalties possible — and barred from the securities industry for life. And, I wish that a jury could hear from the THOUSANDS OF VICTIM(S) of Naked Short Selling. There are so many companies that have been targeted and victimized by these Financial Rapists.

Mr. Mitchell, I know you are the only investigative journalist that is exposing these financial criminals. I challenge any ethical member of the press/media/journalism that is reading this excellent investigative journalism by Mr. Mitchell — to join the cause of JUSTICE — and help Mr. Mitchell to expose the corrupt financial criminals so that justice can be swiftly delivered.

I cannot thank you enough Mr. Mitchell for what you are doing! And, thanks to Dr. Patrick Byrne, CEO of Overstock.com, for making this blog and investigative journalism possible.

Mr. Mitchell, please continue to drag and expose these corrupt criminals into the spotlight of justice. I check this blog daily to see more of your excellent investigative journalism. Thank you sir.

May God Bless,

Hang_’em_High

Well said Hang_’em_High.

There’s an article on silverseek by Theodore Butler that suggests the Commodity Futures Trading Commission (CFTC) looked the other way during JPMorganChase takeover of Bear Stearns, covering up a huge short position in silver bullion futures in the process. Capture in all markets.

Also, anyone catch that Eric Holder has accepted the position of Attorney General-Elect? AKA Mr. Favorable Opinion for Clinton to Pardon Marc Rich?

Thanks for your continued efforts in exposing those, in and out of government, who would attempt to destroy our markets. I too, which that there were other journalist with your integrity who would get involved.

Many thanks also to Patrick, EB, Mark, David, Jonathon, Bud and all those many small investors who write letters to the SEC, Congress, etc.

Maybe the new administration will be more receptive to cleaning up the mess, though I wonder if there will be anything left besides massive debt for you and I, and mansions and the good life for the crooks. Up till now it appears that crime does pay.

There must be a Pulitzer Prize category for this kind of internet investigative reporting. If not, let them make one and award Deep Capture the prize. This is a no-brainer!

For award submissions:

http://www.pulitzer.org/how_to_enter

For contact:

http://www.pulitzer.org/contact

Perhaps it is worth noting that the lawyer at Debevoise & Plimpton who dealt with SEC’s Paul Berger to get a clean bill of health for John Mack was none other than Mary Jo White, who was President Bill Clinton’s U. S. Attorney for the Southern District of New York (Manhattan). As I recall, in the spirit of bipartisanship, President Bush allowed her to review Clinton’s pardons (Marc Rich, et al.) and she found no problems. Reform from the new administration? Maybe I’ll be surprised.

What do you do to earn that kind of money? Or, have you already earned it?

If what they ‘did’ at the SEC entitles them to this size payday, how much money is involved in naked shorting?

(I already know the answer.)

Mark:

I am certainly pleased to see that you are still bird-dogging this issue and agree with you that short-selling and naked short selling are totally destabilizing the financial markets in the US and elsewhere as the SEC turns a blind eye, or aids and abets the process as we have discussed previously. I also agree with your comment that, “Last month – after naked short selling and other hedge fund tricks contributed to the biggest financial cataclysm since 1929 – the SEC inspector general issued a 191-page report confirming just about everything in the U.S. Senate reports. It is impossible to read these reports without concluding that this is the biggest scandal in the history of the SEC–a scandal that entailed a cover-up of precisely those same crimes that “severely injured” (or rather, nearly vaporized) our financial markets.” As you know, I think that the Chairman of the SEC is a lamebrain and in the pocket of the hedge funds which began with his removal of Rule 10(a) from the SEC Act of 1934 to allow unrestricted short selling.

The so-called “de-leveraging” that the hedge funds are going through recently to try to recoup asset values for their wealthy clients is a coverup for their continued short-selling and naked short selling as evidenced by the explosion in FTD’s. Why else would the DOW have declined by 9.67% in the month of October alone if the hedge funds were only dumping securities they already owned long?

How do we get your information in front of the investing public that the SEC’s inaction is depleting their 401(k) accounts, destroying their pension funds, and destroying their retirement plans? Hopefully, the federal district court that you mentioned will get to the facts in the SEC scandal (even though the SEC is doctoring evidence), but is there any way to get it into the press? I would think that the liberal press (i.e. NY Times, Washington Post) would love a story about scandal at this level of government. Another concern is Eric Holder as the new Attorney General. I doubt if he would pursue this issue.

What a quandry, but keep up the good work.

Bill Gardner

This is fantastic investigative journalism. This is the real deal. Thanks Mark,

Tom

Mark, nothing more to add other than a sincere “tip of my hat”. Thanks for your time and effort and to all others doing the same.

AMG

NO BULL IN THE CHINA CLOSET

We cry out for mainstream coverage to expose these criminals…but sometimes we just need to cry out.

http://www.dailypaul.com/node/55223#comment-784769

Relish the catharsis.

Told you so !!!

Hi Mark,

I too would like to thank you for your continuing effort to expose the counterfeiting hedge funds industry and the SEC support they have been receiving.

When I ask myself HOW any member of Congress could ever think that the Rich and Powerful who setup the hedge fund industry did not need any regulation, and would not be affect by greed, and would never do anything illegal to increase the value of their bank accounts, I come to the conclusion that no sane Congress person would ever conclude any of these things were true. Yet we see that Congress continue to support the non-regulation of the hedge funds by their actions. And we see the SEC continuing to put band-aids on the acknowledged counterfeit shorting problem, which actions show us they refuse to take concrete steps to stop this counterfeiting.

With your efforts and those of many others, such as, Dr. Byrne, there is some hope that justice may one day prevail.

Thank you.

Now if it hurts them its serious huh?

Wachtell Lipton Calls for Return of Uptick Rule

NOVEMBER 20, 2008, 12:34 PM Link to This

E-mail This TOPICS Legal INDUSTRIES Financial Services As shares of Citigroup, Blackstone and other heavyweights of the finance industry slumped to new lows on Thursday, a prominent law firm passionately repeated its call for the reinstatement of the “uptick rule.”

Wachtell, Lipton, Rosen & Katz, a firm whose client list reads like a Who’s Who of corporate America, said in a memo to clients that the “very same conditions that led to the adoption of the Rule in 1938 exist today” and sharply criticized the Securities and Exchange Commission, and its chairman, Christopher Cox, for failing to act sooner. “There is no tomorrow,” the memo said.

The uptick rule was created in an attempt to prevent short-sellers — who bet that a given stock will fall — from causing a selloff in shares that were already declining. The rule, which only allowed short sales on a stock whose last trade was higher than the previous one, was abolished last year. Many believe its removal has seriously destabilized the markets, though there is not universal agreement on this point.

Read the full text of the memo below:

November 20, 2008

Reinstate the “Uptick Rule”

The worldwide securities and credit markets continue to experience unprecedented meltdowns and volatility. Millions of investors are losing their life savings and retirement assets. There continues to be widespread manipulative short selling and bear raids. The investing public is losing confidence in the integrity of our markets.

For the past 5 months, we have called on the SEC to reinstate the “Uptick Rule” which helps limit downward spirals by allowing a stock to be sold short only after a rise from its immediately prior price. Despite widespread market participants’ calls to do so, the SEC has failed to act. The SEC must reinstate the Uptick Rule now to address the short selling, bear raids, and the spreading of false rumors. Nearly all the reasons that the SEC gave for repealing the Uptick Rule in July 2007 are not valid in today’s turbulent markets. In fact, the very same conditions that led to the adoption of the Rule in 1938 exist today.

Historically, the SEC has placed a leadership role during market crises to assure that the markets are fair and orderly. The SEC has not hesitated in the past to be creative and innovative in protecting the securities markets and the financial intermediaries from manipulative conduct. Decisive action cannot await the appointment of a new SEC Chairman. The SEC must take a leadership role in restoring investor confidence. It is long overdue. The SEC and Chairman Cox must act now. There is no tomorrow. The failure to reinstate the Uptick Rule is not acceptable.

Edward D. Herlihy

Theodore A. Levine

http://amlawdaily.typepad.com/amlawdaily/files/reinstate_the_uptick_rule.pdf

This letter from Wachtell, Lipton, Rosen & Katz reminds me of my previous suggestion about filing a class action lawsuit against the SEC for giving Market Makers the right to issue new shares of stock without the approval of their Board of Directors and Stockholders.

I am wondering if it would better for Corporate America to file such a class action lawsuit, since it is their stock that the SEC is allowing market makers to counterfeit?

Tons of buying at the ask , and the ask goes down. God help us sheep ! Please continue to expose these criminals , If we dont , This great nation will be destroyed. This is a war on ” Financial Terrorism “. Blessings !

Who get’s the money from the counterfeit shares?

As is usual the counterfeiters do.

http://www.portfolio.com/news-markets/top-5/2008/12/10/Samberg-Pequot-Zilkha-Mack#page1