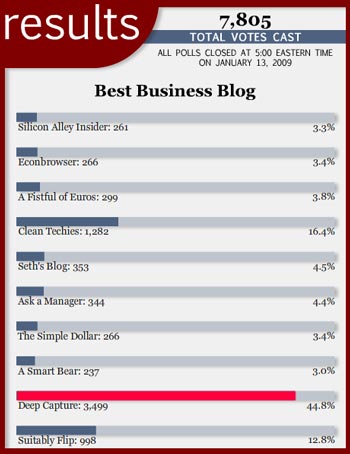

Though the results will not be certified until Thursday, January 15, it would appear Deep Capture will be named Best Business Blog of 2008, and by a rather comfortable margin.

Though the results will not be certified until Thursday, January 15, it would appear Deep Capture will be named Best Business Blog of 2008, and by a rather comfortable margin.

Related Posts

Grok Researches & Reveals the Truth Patrick Byrne

Author’s note: In 2006 -2008 the online British firm TheRegister.com documented in a series of articles that while…

Professor J. Halderman’s Public Affidavits and Declarations to a Federal Court in Georgia

Note: This has been amended to included multiple states of Professor Halderman. This was filed 15 months before…

Manufacturing Consent Regarding “The Big Lie”: MSM’s Biggest Lie of All

Noam Chomsky claims that the Mainstream Media often “manufactures consent” around what is nothing more than blue-smoke-and-mirror narratives.…

A Short (9 minute) Course in Political Philosophy

In nine minutes you can learn a framework into which to fit political philosophers. For extra credit, stick…

Great job guys, you deserve it!

Keep the insights and openings of our minds coming, we need those facts…

Congratulations to Patrick and the entire Deep Capture team. You guys are the greatest, as is plain to see. Thanks to the person who made the nomination, and to all those who voted early and often.

Great Job!

To be frank, I had never heard of Deep Capture before the WebLogs competition.

I am more than intrigued by the courageous stance and well researched investigations into controversial issues here. Hopefully winning this – whatever it is – has brought your sterling work to a wider audience.

It will be interesting indeed to see if any MSM players pick up on your themes.

Well done guys.

What is so impressive is the margin of the win. Way more votes than any others. The dialogue is intelligent and informative. The participants are passionate about an important subject area. What comes across is a love of our country and real pain at what we see happening.

Deepcapture, a blog trying to save the USA, should have Millions of Votes,. Its Sad that Americans care more about whats on TV then this problem that will soon have them thrown in the street unless we do something. Thanks again to deepcapture team for trying to save my family from this National Disgrace

My name say it all to the scumbags destroying this country. Keep up the best expose website available.and bring this country back to the people.

Deep Capture Team,

For the first time I feel my vote was legitimate and counted fairly. I pray for a wider audience, more main stream media coverage and courage to those who are in the know of what goes on behind closed doors and curtains of secrecy to come forward for the sake of their country. Thanks for many hours of endless reading, writing and composition you provide to educate the masses.

Bravo!

R101

A suggestion for improvement:

In addition to comments in response to postings by the DC team, how about a general comment string with most recent comment at the top. It would be a go-to destination for those who want to see the thinking of many of the good outside commenters – and of course, some off-the-wall ones – in response to developments in a timeline fashion. It would help keep comments in response to postings on topic.

Congratulations Patrick, and the entire staff and contributors of deepcapture.com. You have a lot of supporters who appreciate your efforts to fight the good fight against Naked Short Selling and Counterfeit Stocks!

Thank You so much! JustJanet

Great Job Patrick…..break a leg !!

Don’t know which blog I should post this on but I know it belongs withinthe deepcapture series..

Lennar adds Minkow to extortion lawsuitFont size: A | A | A10:42 AM ET 1/14/09 | Marketwatch

RELATED QUOTES

10:37 AM ET 1/14/09

Symbol Last % Chg

LEN 8.09 -6.58%

Quotes delayed at least 15 minutes

BOSTON (MarketWatch) — Lennar Corp. on Wednesday said it has named Barry Minkow and his firm, Fraud Discovery Inc., as additional defendants in a lawsuit against Nicolas Marsch III alleging libel, extortion and various criminal acts against Lennar. Minkow last week alleged Lennar treated its joint ventures like a Ponzi scheme, and the allegations contributed to a 20% decline in the home builder’s stock on Friday. Lennar on Wednesday said Minkow has been operating as an agent for Marsch, who paid Minkow for his services. “Lennar is taking all necessary and appropriate action to protect its investors and shareholders from the dissemination of false and scurrilous claims about the company,” the builder said in a statement.

I am spreading the contact information to anyone who will listen, Last week I passed out info at a local gun show. Go where the people are and help spread the word. This is our last chance to be vigilant about saving our freedoms and country. It is our responsibility. To do nothing is to accept defeat.

Congratulations on this award!

This blog is the definitive story on the love affair of the SEC, Wall Street and the confederacy of suit-wearing dunces in politics.

Keep up the great work.

I encourage each and everyone to engage their online local newspapers ( online) if applicable as I did to spread the word. Each day nefarious behavior regarding market manipulation and corruption by the little guys makes it into your local news. If the article can be applied to Deep Capture, place a link in the comments section. Local government and corruption among officials would suffice as it involves the lower levels of government and works itself up to the top where it trickles down from. Help spread the word. This is NOT a Republican or Democratic thing, it is a GREED thing.

R101

Wow, thats a really clever way of tnhkinig about it!

I am spreading the contact information to anyone who will listen, Last week I passed out info at a local gun show.

Priceless, Diane! Just Priceless. We should have thought of this years ago.

I agree with Reporter101. I’ve found it easy to have letters to the editor of the local paper published as it gets under the radar of the owners of the chain.

Another thought – is there a copyright on the Deepcapture story? If not, and you made it clear that it could be republished for free, some alternative magazines and papers would run the entire story.

If you give us the go ahead, we can all write to the alternative press and ask them to run the Deep Capture story.

Dear Deep Capture Team,

Thank you so much for all your research and hard work. This blog has provided me with much insight. I enjoy reading all the comments and appreciate all the information provided by everyone participating.

You got my vote and I’m looking forward to any updates.

JK

It’s nice to win once in a while.

Well deserved !!!

Inept is onto something. Dr. DeCosta’s last two posts were really good, but they are lost now that this is the active blog.

It would be good if there was someway to keep previous comments, even if they were from the last blog post.

I also agree with Inept… actually he strikes me as quite “ept.” Having a separate, general comments column would streamline the site considerably. Perhaps it is time for a Deep Capture discussion forum with threads, etc… or anything else that will help get the word out and encourage wider participation.

My heartiest congratulations to Patrick et. al. for some well-deserved recognition. It should be noted that not only is it the best business blog but it is most assuredly the business blog with the highest moral calling of any.

More from the archives: Another caveat to management teams: Never, never, never acquire the shares of a publicly-traded corporation (trading in the U.S.) via a “share swap” tender offer involving your own shares. Why? Because the NSCC is going to secretly convert the failures to deliver (FTDs) in the company to be acquired into FTDs (and the incredibly damaging readily sellable “securities entitlements” they procreate) of your own corporation.

Why is this? Because in the case of a “share swap” tender offer of a U.S. corporation with a massive preexisting naked short position the NSCC has three options. They can take one of two proper courses of action or they can commit a new fraud to cover up the existence of their prior fraud. The first proper course of action would be to order the buying-in of all of the FTDs of the company to be acquired in order to level out the books prior to the “share swap”. This would protect the investors of the acquiring company from being defrauded by inheriting the causative agents (“securities entitlements”) from a previously fraud committed against the shareholders of the company to be acquired. They refuse to do this because it would cost their abusive participants a fortune in the case of “short squeezes” and every U.S.-domiciled corporation would follow suit to cleanse their share structures of this toxic waste in the form of readily sellable “securities entitlements”.

Another proper course of action would be to warn the acquiring company’s management, BOD and voting shareholders of the existence of all of this toxic waste they’re about to “inherit” should they vote positively for the tender offer. They can’t do this either because it would reveal the existence of the underlying fraud involving our clearance and settlement system being illegally based upon “collateralization versus payment” which has resulted in abusive DTCC participants intentionally killing U.S. corporations for financial gain. Since the NSCC refuses to do either of the two proper courses of action they in essence relegate all acquiring corporations of U.S. corporations via “share swaps” to be blindly buying a “pig in a poke”.

After refusing to take either of the two proper courses of action the NSCC always opts to take the fraudulent course of action. As we know “fraud” involves the intentional use of “deceit” usually for monetary reasons. The NSCC always opts to knowingly deceive the management, BOD and voting shareholders of the acquiring company to the detriment of their shareholders and employees in order to save their own “participants” the monetary expense of covering their “open short positions” and to avoid admitting to the world that our markets are “rigged” in favor of abusive DTCC participants and their hedge fund “guests” able to place and collateralize massive naked short positions.

Refusing to admit to the prospective investors of the world and to the shareholders of all acquiring corporations of the “rigged” nature of our clearance and settlement system is a form of a “cover up fraud” while the use of deceit in protecting the financial interests of their abusive participants via circumventing possible “short squeezes” is a form of garden variety “fraud”.

The refusal of acquiring corporations with well-educated management teams to acquire U.S. corporations via “share swaps” is yet another form of damage being incurred by investors desirous of tender offers at levels above current share price levels.

Why are all of these layers of deceit necessary and cover up frauds necessary? Unfortunately for unknowing investors the very foundation of our DTCC-administered clearance and settlement system is based upon the concept of “collateralization versus payment” (CVP) instead of the congressionally mandated “delivery versus payment” (DVP) associated with the “prompt settlement” of all securities transactions. In CVP the sellers of nonexistent shares are merely asked to collateralize the monetary amount of their failed delivery obligations before they are allowed to gain access to the funds of naïve investors inaccurately assuming that these markets are highly regulated.

Since failures to deliver (FTDs) result in incredibly damaging and readily sellable “securities entitlements” the share prices of corporations targeted for an attack can easily be placed into a “death spiral” downwards. Since the collateralization requirements go down as the share price predictably tumbles then the investor’s money is unconscionably allowed to flow to the abusive naked short sellers that absolutely refuse to deliver that which they sell.

Since the very foundation of our clearance and settlement system is and has been based upon fraud the clever Wall Streeters and their hedge fund “guests” aware of this fraudulent foundation have amassed massive amounts of intentional or “strategic” delivery failures (Dr. Leslie Boni 2004) over the years. This fraudulent behavior has gotten so far out of hand that the SEC admitted that the en masse buying-in of these FTDs might result in undesirable market volatility (short squeezes).

Due to the nature of this fraud the NSCC has been given the unenviable task of either buying-in the delivery failures of its abusive DTCC participants or continue to cover up and deny the very existence of the fraud and these “open naked short positions” that are currently crippling the share prices of the corporations unfortunate enough to be targeted for an attack. As in the case of the “share swap” tender offer cited above the NSCC was given two proper choices and one fraudulent choice to remedy this dilemma.

Prior fraudulent behavior that has gone unchecked for extended periods of time like that associated with abusive naked short selling frauds leave us with two clear cut choices. You either address it when it is discovered (now) or you willfully choose to deny it, willfully choose to continue to commit the same fraud and willfully commit to perpetrate further cover up frauds to hide the existence of the original fraud. If you choose not to address it NOW upon its discovery then the number of victims of the original fraud plus the cover up frauds will grow geometrically not arithmetically.

Mandated buy-ins will address both the preexisting frauds as well as provide the heretofore missing truly meaningful deterrence to dissuade the commission of future frauds. There is no longer any safe middle ground for the NSCC, FINRA or the SEC. You’re either part of the solution or the cover up.

Congratulations to Patrick, Mark & Judd and the entire Deep Capture team and all the participants for making Deep Capture the “Best Business Blog” on the internet! You are all American Heros — for standing up against the financial thug criminals.

Deep Capture is the only source for REAL INVESTIGATIVE JOURNALISM that has exposed the fraud, corruption and manipulative-abuse of Naked Short Selling. This is so important — because of the severe damage being inflicted to companies, their employees and their investors which have all been targeted by Naked Short Sellers. From a macro perspective, everyone is affected — because fraud and corruption reduces confidence in the overall market.

The “Best Business Blog” Award will help elevate DeepCapture.com as the most urgently-important blog on the internet — because so much is at stake — to stop the perpetrators of financial crimes. After all, it’s everyone’s 401(k) retirement, I.R.A. and financial market investments — which are on-the-line.

Because the regulators, elected-officials and New York financial media (print & TV) are influenced (DEEPLY CAPTURED) by the perpetrators of Naked Short Selling, LITTLE TO NOTHING HAS BEEN DONE TO STOP THE PERPETRATORS…and they continue to inflict damage on a daily basis.

By PUBLICLY-EXPOSING the perpetrators of fraud and corruption involved in Naked Short Selling, the DeepCapture.com Blog is performing a great service — giving us all “hope” that sooner or later the regulators and elected-officials will TAKE-ACTION to protect investors.

Let’s all keep the pressure on local media — to print the DeepCapture.com Story — and publicly-expose the fraud and corruption. We must surround the perpetrators from all angles — starting with a grass-roots publicity campaign.

In the future, I would like to know of actionable-ways that we can all work together for maximum-effect — to get legislated the reforms urgently-needed to SAVE (I believe this is the correct word at this jucture) the financial markets from destruction.

In my opinion, the blog entry by Patrick, titled “So You Say You Want A Revolution?” (linked below), provides email contact lists and guidelines to make the necessary contacts — to make the public aware of the gravity of the fraud and corruption that is currently damaging financial markets. Let us all fill up the “Inbox” of EVERY newspaper reporter in this country. If we “all” do this, then I believe action will be taken to protect investors from the financial thugs destroying our markets.

https://www.deepcapture.com/so-you-say-you-want-a-revolution/

Together, the Deep Capture participants are a force for positive change in this great country. At this point, our country has been taken hostage internally by the financial thugs that have corrupted the system. NOW, we must fight back — to cleanse the financial system of these criminals — and return the financial markets to a “level” playing field.

I refuse to call myself a “victim” — because I will be VICTORIOUS over my enemies – the financial thugs doing the Naked Short Selling.

I know that I cannot effect change by myself, but together, we can make it happen.

Hang_’em_High

Would anyone care to comment on or postulate on today’s option activity in Fairfax, (Patchie?) common sense tells me something is afoot with sir(s) shorts-alot. alas since I don’t run in hedge fund or market making circles, i can only guess.

All right! Enough backslapping. Back to work everyone.

Question for anyone out there? We have freedom of information act. Since the gov. bailed out all these banks some that own part of the DTCC and things. Would the Freedom of information act work against the DTCC since so many of the banks are being taken over by the government. Or would we have to wait until a complete gov. take over of the DTCC?

YIPIKAYE

Mark Cuban asks for dismissal of SEC chargesFont size: A | A | A10:41 AM ET 1/15/09 | Marketwatch

SAN FRANCISCO (MarketWatch) — High-profile investor Mark Cuban asked for the Securities and Exchange Commission’s insider trading charges against him to be dropped, arguing that the regulator’s suit is a “test case” for a flawed legal theory.

The SEC filed suit against Cuban in November, alleging he sold shares of Internet company Mamma.com based on non-public information, thus sparing himself hundreds of thousands of dollars in losses. See related story on SEC charges against Mark Cuban.

The SEC alleges that in 2004, Cuban promised to keep information about Mamma.com’s impending secondary stock offering confidential, though he sold his stake in the company before the offering’s disclosure sent shares in Mamma.com falling.

However, Cuban argued in a motion filed late Wednesday in a Texas federal court that the SEC is at odds with the established law of the land.

“There is no general prohibition on the trading of securities based on material, nonpublic information,” Cuban argues in the filing. “Although the SEC has often argued that any recipient of material, nonpublic information has potential insider trading liability, the U.S. Supreme Court has repeatedly rejected the SEC’s view.”

Cuban asks that the suit against him be dismissed with prejudice.

Cuban, the billionaire owner of the Dallas Mavericks NBA basketball team and prolific chronicler of his own life on the Internet, said in the filing that, rather than keeping his sale of Mamma.com shares secret, he “openly disclosed both his sale of Mamma.com shares and his reasons for selling.”

In addition, rather than a corporate insider, Cuban argues that he was merely a “minority shareholder who was owed a fiduciary duty by Mamma.com’s officers” at the time he discussed the planned secondary stock offering with the company.

Cuban held a 6% ownership stake in Mamma.com before selling his shares.

If the SEC’s charges are upheld, Cuban could be forced to pay millions of dollars in disgorgement and penalties.

Oh com’on. what a scam. i’ve been trapsing around the blogsphere for well over a year now and i’ve never heard of deep capture until about a week ago. nobody links to it. nobody cites it. there’s no way those results are good. i wouldn’t doubt it if someone set up a macro that just kept deleting cookies and then re-voted for this site.’

someone needs to do a deep capture on deep capture.

someone needs to do a deep capture on deep capture.

Spyro? Is that you?

No its Barry!!

Or Gary ?

“nobody cites it”

go to every high traffic blog…see for yourself…calculated risk, naked captialism, econobrowser…”deep capture” isn’t in their blog roll. those authors work very hard for their traffic, too. but to say that deep capture is more popular by a factor of 10 is way too much for a newbie, like myself to believe. so i sit here and question how biased this cite is. i want to believe that its real because i like this site as its unique and uncovers crappy journalists. but seriously, if you guys play the same games as those idiots (lilke pumping your own popularity), why should i trust anything you say?

the fact that i question that eggregious statistical outcome…especially since there is little or no transparency to the way the vote is conducted…should not be a surprise to people that enjoy this site. questioning the opacity is what its all about. so thats what im doing.

seriously, a statistical abberration of that size should be immediately questioned. and it bugs me that more readers arent asking that question.

and by the way “best business blog”…awarded by whom?? theres no name for who conducted the survey…links please???

anon,

You want links because you’re skeptical about the conclusions of DeepCapture?

http://www.counterfeit-o-meter.com/stories/

You want links to show the legitimacy of the webblog awards?

http://weblogawards.org/

You’re welcome!

thanks for posting the weblog awards site. but i can’t find a methodology for how they compile votes…is it possible that someone can sit there and delete cookies and re vote dozens of times over?

i’m afraid that deep capture is too skewed or fanatical to take a measured approach and if something doesn’t fit it will bend or force stuff to fit a conclusion. that’s a hurdle this blog should be pathelogically self aware of.

fanatacism scares me as im sure it does others. similar to the way michael moore scares me. as much as gw was the worst prez ever, i dont’ trust michael moore to tell me the whole truth more than i can throw him.

as much as i distrust hedge funds and business media, i’m not about to start trusting those vote numbers.

to unequivacoblly accept those aberrational vote outcome as dogma is contrary to everything this blog seems to stand for.

“but i can’t find a methodology for how they compile votes…is it possible that someone can sit there and delete cookies and re vote dozens of times over?”

simple, contact the admins there and do analysis on there logs.

“as much as i distrust hedge funds and business media, i’m not about to start trusting those vote numbers.”

you’ve already made up your mind.

no. why don’t YOU do the analysis. that’s what i’m trying to tell you. the fact that i’m having to pry it out of you…despite the aberrational nature is disconcerting, to say the least. just let your readers know that it wasn’t rigged. if i’m were a perfect representative of your readers, then they would be highly skeptical of this type of aberration.

sorry paul…i was assuming you were the moderator…i mean why doesnt Judd do the analysis.

Anon, while the other blogs you mentioned may be excellent and have plenty of traffic, I don’t see any of them on the list of options to vote for. I don’t know if that means they weren’t nominated or simply didn’t get enough votes in an earlier round or what, but it would seem difficult for them to get more votes than Deep Capture if votes can’t even be cast for them to begin with.

Beyond that, if we were talking about tens or hundreds of thousands of votes, you may have a point regarding the wide margin of victory. But given we’re only talking about a few thousand, have you considered perhaps that the other candidates on the list, while good and informative, simply don’t inspire the kind of deep feelings the Deep Capture story does? Most people driven here have probably been victimized in one way or the other to the tune of thousands of dollars by abusive naked short selling hedge funds. Of course those people are going to do whatever they can to promote this blog. Can the other blogs say the same? Even if Calculated Risk, which I read daily and think is a very valuable resource, were on the list, would I go back and vote for it daily? Not likely. It just doesn’t matter that much to me. Did I go vote daily for this one? You bet you sweet bippy I did. I own FFH, BCON, CPST, ENER, and EEEI. I’ve been positively hammered by these crooks over the last couple years. What I read here scares the living hell out of me and I want everybody to understand this story. I have no trouble believing most readers here feel the same way.

And I have even less trouble believing someone who would come here making the complaints you’re making now has some ulterior motive for doing so.

redwood…i’m in the same boat as you. and i’m not surprised that you think i have ulterior motives (as i am in the skeptical camp, like you). but what i am surprised about is that nobody is questioning the vote nor offering more detailed stats. SAI has a huge presence (at least in my mind)…i have no stats to back that up, but i don’t care to have those stats…thats the beauty of the blogsphere…i dont’ have time to do an analysis….other than the hope that this blog is what it says it is, i haven’t committed anything, nor do i want to…blogs that take the time to analyze aberrational statements – regardless of if they are flattering or not – are the blogs that i stick to. other people might have other standards. but i think that its a reasonable standard, to say the least. just sticking to something because they are telling you what you want to hear is ridiculous. so for heavens sakes somebody just show that 2000 votes didn’t come from one address.

HEDGE FUNDS AND ABUSIVE NAKED SHORT SELLING

I’ve always gotten a kick out of the argument of hedge fund managers that they need not be regulated. They proffer the argument that their investors are “financially sophisticated” and “accredited” investors that don’t need the “investor protection” theoretically provided by the SEC. Although Bernie Madoff didn’t technically run a hedge fund we did learn that even the most financially sophisticated people on the planet do indeed need “investor protection” from financial frauds.

Another argument proffered by hedge fund managers is that their trading activity deserves an extra layer of secrecy over and above that owed to the rest of us. They assert that their sophisticated “proprietary trading methodologies” (“black box methodologies”) that they have developed might be stolen and imitated by other investors. That never made a lot of sense to me. If the research of their brilliant analysts resulted in their taking a long or short position in a certain security wouldn’t they want to announce that from the mountain tops so that other investors that recognize their brilliance would follow suit and place like bets which would naturally enhance the prognosis for the bets they placed. Why the obsession with secrecy? Why would a hedge fund already based out of the banking secrecy obsessed Cayman Islands need yet more layers of secrecy above and beyond that accorded to less politically powerful and less financially sophisticated investors?

One explanation for their obsession with secrecy might be associated with the hypothesis that for some hedge funds their “proprietary trading methodologies” involve fraud and that they were “levering” some sort of advantage they can access over regular investors that they and their co-conspirators were “entrusted” not to take advantage of.

What advantages do hedge fund managers have over Joe Sixpack that they might be tempted to lever? Hedge fund managers collectively have about $11.2 billion to spend annually on the DTCC participants willing to be the most “accommodative’ to the needs of the hedge fund manager making his “2 and 20” (2% of assets under management and 20% of the profits).

In abusive naked short selling frauds one of the main DTCC participating “market intermediaries” that hedge fund managers want to befriend is the “abusive market maker”. Why is this? It has to do with a gigantic loophole in our clearance and settlement system that allows theoretically “bona fide” MMs to access an exemption from pre-borrowing or making a “locate” of borrowable shares BEFORE they make admittedly naked short sales. The theory is that a bona fide MM doesn’t have the time needed to effect a pre-borrow or “locate” in fast moving markets while he is injecting all of this theoretically beneficial “liquidity”. Accessing this exemption for a corrupt hedge fund is especially financially beneficial when the shares of the corporation under attack are “hard to borrow” which is synonymous with “expensive to borrow” as any borrow can be easily circumvented.

Note that in abusive naked short selling (ANSS) frauds there is no limit to the number of “securities entitlements” resulting from FTDs that you can poison the share structure of a targeted company with. In legal short selling there is a built-in “governor” in that there are a finite number of legally borrowable shares available and once they’re all loaned out then that’s it. Actually “that’s it” is not accurate as that is typically when the ANSS fraud takes over. Note that in legal short selling there is also a natural deterrent to these crimes as when the supply of legally borrowable shares tightens up the “rental rate” gets higher via supply and demand interactions. This might dissuade short sellers from assuming new short positions associated with the increased expense which changes the risk/reward calculus. ANSS methodologies wipe out all of the “natural” market deterrents to these activities.

How does a corrupt hedge fund gain access to this incredibly powerful but universally abused exemption without getting busted by the cops? Instead of cash bribes it simply directs “order flow” to any MM willing to “rent out” some of that space under the “umbrella of immunity” from making pre-borrows or “locates”. Do you recall how Gov. Blagojevich just knew he had a financial windfall available with his ability to appoint someone to the vacant senate seat. He’s got nothing over abusive MMs! Since “order flow” to an abusive MM represents “cash flow” indirectly then the cash proceeds from this illegal behavior is essentially “laundered”. But doesn’t a hedge fund have the right to direct “order flow” to any market intermediary it so chooses? Sure they do as long as it doesn’t directly or indirectly involve a “quid pro quo” involving the defrauding of average investors.

What other sources of “leverage” can a hedge fund manager access? In a clearance and settlement system illegally based upon mere “collateralization versus payment” (CVP) instead of “delivery versus payment” (DVP) any illegal naked short positions assumed merely need to be collateralized on a daily marked to market fashion. But remember these initial collateralization requirements can easily be lessened by predictably placing the share price of the corporation under attack into a “death spiral” simply by simply refusing to deliver that which you sell and drowning the corporation’s share structure in readily sellable but incredibly damaging “securities entitlements”. How much trouble would a $10 billion hedge fund leveraged with borrowed money at 10-to-1 via its prime broker have in merely collateralizing the monetary value of an ever-diminishing failed delivery obligation? To exacerbate this “leverage” keep in mind that the collateralization requirements being returned to the sellers of nonexistent shares with each downtick in the share price of the targeted company can then be used to collateralize that much higher of an illegal naked short position. Note the self-fulfilling prophecy to this particular version of a “fraud on the market” known as ANSS.

Can Joe Sixpack take part in these frauds? No, Joe is neither a member of the DTCC’s NSCC subdivision nor does he have the financial wherewithal to direct massive amounts of order flow to abusive MMs willing to illegally access that exemption accorded only to truly bona fide MMs. Note that a truly bona fide MM that can legally access that exemption will cover any naked short position that he established on the next downtick when “liquidity” is in need of being injected from the buy side.

As history has clearly shown us the abusive MMs that illegally accessed this exemption are nowhere to be found when it comes time to cover these naked short positions as the share price “tanks”. Why is this? Because in a clearance and settlement system unconscionably based on CVP you’re allowed to gain access to the unknowing investor’s funds even without ever delivering that which you sell. One would be insane to EVER cover a naked short position in an environment like that. Why would one ever go to the expense of buying something before you sell it when you’re granted access to the investor’s money without buying or delivering anything?

Does the fact that the largest donors to the political campaigns of the politicians that oversee the SEC play a role in all of this? Who knows?

Do the hedge fund managers pleading for no regulatory oversight ever express any concern for the “systemic risk” implications of their use of leverage as they swing for the fences on investments in order to beef up their (“2 and 20”)? Do they have any qualms about the fact that the “systemic risk” associated with the abuse of leverage for greed’s sake eventually lies on the shoulders of the investors they are defrauding in abusive naked short selling attacks? I think we all remember the painful “deleveraging” process we recently experienced when self-centered hedge fund managers swinging for the fences with borrowed money were forced to sell everything in sight in order to “deleverage” their abuses of leverage. Note that when markets go upwards the hedge fund manager makes a fortune with leverage but when markets go down WE ALL PAY.

Have you ever wondered why wealthy investors would pay the usurious rates of 2% of assets under management and 20% of the profits? Don’t those investing large amounts of money usually get a “volume discount” rate? The answer lies in the fact that in order to gain access to this “cycle of corruption” and the associated “self-fulfilling prophecy” you need enough critical mass to direct order flow to the abusive DTCC participating market intermediaries (especially abusive MMs, prime brokers and clearing firms) willing to prostitute the superior knowledge of, access to and visibility of the clearance and settlement system that they were ENTRUSTED not to leverage. You need to be able to “juice” the right market intermediaries; after all there’s plenty of naïve investor money to go around if everybody just plays their role and nobody “rocks the boat” by ordering the buying-in of any of the FTDs actively manipulating downwards the share price of the corporation under attack.

In the discussions of the need or lack of need for hedge fund regulation the SEC needs to realize that it’s not the wealthy “accredited” investors in the hedge funds that necessarily need the “investor protection” and be the focus of this issue. It’s the average investor that unfortunately took a “long” position in a security that hedge fund managers and abusive market makers willfully targeted for destruction by abusive naked short selling that needs the help.

“i dont’ have time to do an analysis….other than the hope that this blog is what it says it is, i haven’t committed anything, nor do i want to”

So anon, you don’t have time to do an analysis, but, you come here questioning the validity of the vote itself ( wrong place to get that information in the first place) contact: http://weblogawards.org/

and you also have no time to find out about it and you could care less it seems but you want to question the people who voted daily to do your investigation for you because you raise questions ?

Am I missing something here ? Oh yea,

Hahahahahahahahahahahahaha

reporter,

“due dilligence” is not a bad thing. i view the blogsphere as uniquely leverageable b/c the cream rises to the top. its a meritocracy. i don’t have to spend time doing an analysis b/c i don’t have anything invested (like i do with hard research or magazines or the like). if a simple due dilligence question can’t be answered i just take the blog with a grain of salt. i’m baffled why you wouldn’t.

By all means, do your own DD and report back to us. I’ve done mine already.

Regards,

R101

Had more people done DD in Madoff case, more people would not be out of $$$$$$$$ right now. Taking what I say or anyone else regarding the voting as the gospel is just ridiculous.

I do have a feeder fund you might be interested in investing in. I’ll have my friends call you and tell you just how legit it is as to not waste time you do not have to check for yourself. $1 million minimum. Guaranteed 80% return annually.

Regards,

R101

anon,

I apologize. I am not trying to attack you. I just find it very odd you have no true interest what so ever in this blog and question whether the voting was legit, but, you do not care to find out for yourself ? Different strokes I suppose. Either way, good luck with your question.

R101

On a serious note anon,

Lets take your hypothesis. It can be rigged by deleting cookies and voters can vote many times in the same day. If this were possible, why would the voters for Deep Capture only take advantage of this despicable act ? Would it or could it not apply to votes coming into other nominee’s ? I trust the validity of the votes will be ensured by http://weblogawards.org/ before announcing the winner.

R101

Can someone please answer this question for me ?

**According to this, Madoff may not have made any trades.**

Madoff might not have made any trades

Agency can’t find evidence his funds bought or sold through his brokerage

By Beth Healy, Globe Staff | January 15, 2009

http://www.boston.com/business/articles/2009/01/15/madoff_might_not_have_made_any_trades/

Obama’s SEC Choice Promises Aggressive Action

JANUARY 15, 2009, 12:17 P.M. ET

Associated Press

http://online.wsj.com/article/SB123203844387786085.html

According to this by Ms Shapiro when asked by Dodd about the failure of FINRA in regards to Madoff case she stated:

“Because the alleged fraud was carried out through Mr. Madoff’s investment business, and FINRA was empowered to inspect only the brokerage operation, it wasn’t possible for her organization to discover the violations, Ms. Schapiro said.”

Now, if Madoff didn’t make any trades, and FINRA truly inspected only the brokerage operation, would they have found he didn’t make any trades ?

I smell a RAT…..

R101

Congratulation to DeepCapture.com !!

For those here who have more knowledge about naked shorting, I have a question about how the term “ponzi scheme” might apply.

First here is the definition I found in the online Meriam Webster Dictionary:

>> Pon·zi scheme – an investment swindle in which some early investors are paid off with money put up by later ones in order to encourage more and bigger risks.

My first thoughts when the news about the Madoff “ponzi scheme” hit the news wires was that the term “ponzi scheme” did not apply to naked shorting. Now I am beginning to think that this first thought was NOT CORRECT.

When I consider that “naked shorting” is “illegal counterfeiting,” and that the counterfeiting hedge funds and their supporting cast members might very likely have to declare bankruptcy if they were FORCED to buy in the open market all the counterfeit share they created, then there seems to be some connection between the term “ponzi scheme” and “naked shorting/ counterfeiting”.

Consider this:

“…investors are paid off with money put up by later ones”

Counterfeiting hedge funds are making easy money through counterfeiting and they are NOT explaining to their “new investors” (nor old ones) that they keep a “second set of books” which show the continually rising debt they are daily accruing for converting the counterfeit shares into genuine shares through regulatory mandated “buy-ins”.

Since the counterfeiting hedge funds are hiding their second set of books, and not explaining to investors they are accuring a hiden debt, is not this a type of “ponzi scheme?”

If, according to Ms Shapiro FINRA only checked the brokerage, and investigators are unable to find any evidence his funds bought or sold through his brokerage, is Shapiro saying when they checked the brokerage, they found NO trades and this was not a red flag ?

I just spoke with Beth Healy from Boston Globe and put a bug in her ear about my thoughts. She did say there were trades going through his brokerage, just none of his own. BIG RED FLAG FINRA !!!! Shame on you.

maybe DC can post an rss feed counter…show us how many people have subscribed. If its somewhere near 3.4k, ill give them a pass, i’ll even give them a pass if the ticker shows 1/3 that amount.

anon,

From a post of yours, it appears that you are not aware of the voting rule that allows anyone to vote once every 24 hours during the time period allotted.

This seems to imply that you never voted for any of the blogs in the first place – otherwise, would you not already understand the voting rules?

So you are now complaining after the fact about DeepCapture.com winning, because…. why?????

Anon,

The people who read this blog support it. The writers here expose criminals in the market.

Go read a letter to the SEC from the National Coalition Against Naked Shorting… count the signatures..1000 or so individuals and they all know the issues. If only the most loyal each voted 7 times that would account for 500 people.

The voting over the week stayed proportionally the same. DC hit over 40% the first day and got up to 44% midweek, dropped back and then went up as high as 45% the last day. The other blogs kept their figures about the same all week.

This contest is great because if you are looking for what is considered the best in various area, you can go to the awards site. Some of those that had won for years, were not included in some of the categories.

I really enjoyed learning of such a great resource. These blogs are communities. There are some great communities on the web.

Because the issues that are brought out here have been kept secret by Wall Street and those who want to have special rules, special treat while they violate the law, the writers have been subjected to intimidation and outright threats on their persons… and the people who follow this blog are very protective of the authors and you will not be welcome if you don’t understand or appreciate what has happened in the last many years.

If you read Mark Mitchell’s long piece, it will bring you up to speed. It will take you longer to understand the posts by Dr. DeCosta.

You won’t get investment advice here. You won’t be told how to run a business, but you might learn some things about forming a grassroots movement.

Hope you enjoy our community.

For the past two decades, Wall Street watchers could count on four U.S. firms to land in the middle of every securities scandal. From Nasdaq price fixing to fake research to rigging the IPO markets to peddling toxic subprime assets, one could rest assured that Citigroup’s Smith Barney, Morgan Stanley, Merrill Lynch and Goldman Sachs would be heading the lineup. Their complete absence from the greatest Ponzi scheme in history raises the question: what did they know and when did they know it?

The answer may reside in a pentagonal structure created in 1999 to serve the interests of a Wall Street cartel.

http://www.counterpunch.org/martens01152009.html

1999 was also the year the DTCC was formed. The following year was the big dot com bear market.

Hello,

Does anyone know how I could get a hold of Judd??? He had mentioned awhile back about posting the Fairfax 1000 page court report but have yet to see anything. Thanks for your help

Kyle Holmes

[email protected]

Wow!

Kudos Doc

PT

Need there be anymore said?

Breaking News

•Bank of America Gets $138 Billion in U.S. Funds, Guarantees on Asset Pool

FINRA speaks out. Ms Shapirio has smoe splain’ to do at her confermation hearing. She and her predecessors at FINRA are catching up to SEC incompetence levels:

http://siliconinvestor.advfn.com/readmsg.aspx?msgid=25329037

Officials at the Financial Industry Regulatory Authority, known as FINRA, told The Post that after examining more than 40 years’ worth of financial records from Madoff’s now-defunct broker dealer, there are no signs that Bernard L. Madoff Investment Securities ever traded shares on behalf of the investment-advisory business at the center of the scandal.

“Our investigations of Bernard Madoff’s broker dealership showed no evidence that any shares were ever traded on behalf of his investment advisory business,” a FINRA spokesman said, adding that the regulator has looked at Madoff’s books going back to 1960.

http://www.nypost.com/seven/01162009/business/bernies_fake_trades_150467.htm

k of America posts first loss in 17 years

NEW YORK (Reuters) – Bank of America Corp (BAC.N), posted its first quarterly loss in 17 years on Friday and slashed its dividend, hours after winning a multibillion-dollar lifeline from the U.S. government to help absorb Merrill Lynch, which lost a record $15.31 billion in the quarter.

The dismal results came as the largest U.S. bank faced mounting pressure from investors who questioned how well it will absorb a tidal wave of soured loans in an economy showing no signs of escaping a deep recession.

Bank of America cut its quarterly dividend to a penny from 32 cents, and Chief Executive Kenneth Lewis said net losses may be at or above the fourth-quarter level for several quarters.

“It is difficult to focus on what is going right at this time,” a clearly downbeat Lewis said on a conference call.

But, he added, the “severe” recession and credit crisis “will end some day, and people will remember that our company was there for them in hard times.”

Hours after it won $20 billion in new capital from the government’s $700 billion Troubled Asset Relief Program (TARP), the bank reported a quarterly loss of $1.79 billion, or 48 cents per share, compared with a year-earlier profit of $268 million, or 5 cents.

Lewis sought government help after it became clear that Merrill’s credit losses were far higher than expected, and had threatened last month to scrap the $19.4 billion takeover without government help.

Lewis said the government worried that scuttling the merger could create “serious systemic harm.” He said the Federal Reserve and Treasury Department gave assurances that they would provide necessary help if the merger closed.

Bank of America’s purchase of Merrill Lynch and its July acquisition of Countrywide Financial Corp gave the bank significant exposure to several major areas of the financial system, just as the economy’s decline was accelerating.

“They were probably one of the best banks out there, balance sheet-wise, until they did the Merrill deal,” said Cassandra Toroian, chief investment officer at Bell Rock Capital in Paoli, Pennsylvania, which owns the bank’s shares.

CREDIT LOSSES SKYROCKET

Excluding merger costs, the loss was 44 cents per share. Net revenue rose 22 percent to $15.68 billion.

Analysts, on average, expected profit of 2 cents per share, according to Reuters Estimates.

The bank set aside $8.54 billion for bad loans, up from $6.45 billion in the third quarter and $3.31 billion a year earlier. Net charge-offs nearly tripled from a year earlier to $5.54 billion, or 2.36 percent of average loans and leases.

At Merrill, the loss was $9.62 per share, driven by significant writedowns. Bank of America said it expects the purchase to reduce earnings per share for two years, and still expects $7 billion of cost savings.

With the latest capital infusion, Bank of America has taken $45 billion in TARP money, the same amount as Citigroup Inc (C.N), which won its own rescue package in November.

Citigroup also reported fourth-quarter results on Friday, posting a $8.29 billion loss, and said it plans to separate into two units after its own massive credit losses.

Shares of Bank of America rose 14 cents to $8.46 in premarket trading. Through Thursday, they had fallen more than 81 percent from their 52-week high last February.

GOVERNMENT SHARES IN LOSSES

The rescue package for Bank of America calls for the government to share in losses on $118 billion in residential and commercial mortgages, derivatives and corporate debt. The bank will absorb the first $10 billion of losses, the government the next $10 billion, and the government 90 percent of the rest.

Lewis said the rescue package will help it operate as normally as possible. The bank said it had extended more than $115 billion in new loans in the quarter and was adding mortgage staff to accommodate more refinancings.

“This company will generate huge amounts of profit” when the economy returns to normal, Lewis said.

Bank of America is also struggling with defections of top Merrill executives, including brokerage chief Robert McCann and Greg Fleming, who was expected to run the combined investment bank.

Lewis said he is “happy” that former Merrill Chief Executive John Thain is taking a major role at the bank as head of global banking, securities and wealth management.

Bank of America has said it expects to cut 30,000 to 35,000 jobs over three years following the Merrill merger, on top of 7,500 job losses following the Countrywide acquisition.

(Reporting by Jonathan Stempel and Elinor Comlay; editing by Lisa Von Ahn and Jeffrey Benkoe)

Anon,

I found Dc while researching a hunch that Deutche Bank was behind the global economic failure with their Fund of Funds scam. What I have learned here has activated me to cause others to become informed. I have challenged congress members, writers,working people with 401k losses, foreigners and retirees to read DC and to vote for DC so that others would come here and join the conversation. It is my goal to get 10k people here. I own no stocks. I voted once.

Either take the information that is given freely here and learn, or do nothing and suffer the consequence that awaits us as Americans if we do not take action. It is ours to lose. Do not attempt to derail the conversation. We need all the help we can get.

For over a decade I had the opportunity to arbitrate for both NASD and the NYSE. As the Chairman of an RIA firm I was disqualified just a couple of years ago because of the supposed “conflicts” found in members of RIA firms. That ruling nailed the real reason RIA guys like myself, (fiduciaries) were put out of arbitration panels. We were put out of the process because we did the right thing too many times and cost Wall Street too much money. FINRA and the SEC are a joke.

dean parisian

ChippewaPartners,

Welcome and thank you for sharing your experience with us. Although not surprising, it is nice to hear from someone with first hand knowledge of the injustices we are bound by. I commend you and those alike for doing the right thing. FINRA and the SEC in my opinion are jokes and more. My hope is the curtain on these players get pulled back, the layers peeled and the light shines bright on those responsible.

R101

TWO SETS OF BOOKS?

There is a certain element of “two sets of books” accounting between the DTCC, its “participants” and the investors they serve as “market intermediaries”. Let’s assume that “Acme” has 100 million shares issued and outstanding and that all are held in “street name” at the DTCC.

The “legal/nominal/record” owner of all of these shares is therefore “CEDE and Co. which is the “nominee” of the DTC subdivision of the DTCC (a holding company). Let’s also assume that 10 “participating” clearing firms (participants “A” through “J”) of the NSCC each hold 10 million Acme shares in their “participants shares account”.

Let’s further assume that there are 80 million shares being held in a “failure to deliver” (FTD) status with 8 million of these being held by each of the 10 participating clearing firms. These 80 million incredibly damaging “securities entitlements” are allowed to exist as “long” positions in what are referred to as “C” sub accounts at the NSCC. These 80 million delivery failures result in the procreation of 80 million “securities entitlements” and are referenced on the shareholders of Acme’s monthly brokerage statements as “securities held long”.

For the sake of simplicity let’s assume that there are no delivery failures held outside of the NSCC in an “ex-clearing” arrangement. Let’s further assume that these FTDs were associated with abuses within the NSCC’s “Automated Stock Borrow Program” which we’ve reviewed in depth earlier.

The 10 participating clearing firms will each represent to its clients that it is “holding long” 18 million “securities” related to “Acme” (not necessarily “shares” of Acme) even though they only have 10 million legitimate “shares” of Acme in a paper-certificated form being held in a DTC vault. The 100 million legitimate “shares” of Acme are indeed held in a paper-certificated format. They are not held in the names of the 10 participating clearing firms. Instead they are held in an “omnibus” or “fungible bulk” format giving rise legally to these 10 clearing firms owning a “proportionate interest” in this “fungible bulk”.

“CEDE and Co.” technically “owns” these shares. The transfer agent and registrar of “Acme” which play the critical role of detecting any “counterfeiting” issues in the shares of “Acme” only can see that “CEDE and Co.” owns all of Acme’s shares. They are flying totally blind as far as the detection of any “counterfeiting” issues within the share structure of Acme. Acme’s transfer agent, registrar, shareholders and management team have “entrusted” this prevention of counterfeiting role to the NSCC assuming that there are rigorous checks and balances in place to detect and address any issues related to “counterfeiting”.

When a management team of a corporation under an ANSS attack orders an “SPL” (securities position listing) from the DTCC it will receive a document that lists the 10 clearing firms as holding 10 million shares each. Management will confirm with its transfer agent that there are indeed 100 million “shares” legally outstanding and management will be hoodwinked into thinking that everything is hunky-dory at the DTCC.

They will be wrong and victims of misrepresentation as the DTCC will not inform management of the 80 million delivery failures it holds in its “C” sub accounts as “long positions” which are granted to participants that “donate” shares to the NSCC’s “Automated Stock Borrow Program” or “SBP”. That’s obviously the information being sought but instead the management team receives an intentional misrepresentation of the information being sought after. This is a cover up fraud that needs to be perpetrated in order to hide the existence of the underlying fraud involving 80 million incredibly damaging “securities entitlements” (within full sight of the NSCC) actively forcing the share price of Acme downwards.

There is a curious accounting mechanism involved in the NSCC’s SBP. If a participant donates shares to the SBP and they are chosen to “cure” a delivery failure then the borrowed shares will be sent to the buyer of shares in the trade involving a delivery failure. The buyer’s b/d will be given a “long” position in these shares and these shares will be correctly debited from the “participant’s shares account” of the “donor” firm at the NSCC. This all makes sense. Curiously though the donor of shares is awarded a “long” position in a newly established NSCC C sub account in that donating firm’s name. Curiously these accounts are kept out of the investing public’s or management team’s view. The question arises as to how a management team or BOD can manage a U.S. corporation when they aren’t allowed to see how many readily sellable “shares and/or “securities entitlements” their corporation has “outstanding”. For instance, wouldn’t a corporation with cash in hand and the knowledge that they have a gazillion bogus securities entitlements floating around damaging their share structure opt to buy back their shares out of the open market instead of building a new factory?

The DTCC informs us that this “long” position credited to the donating firm’s C sub account signifies that the donor of the borrowed shares has the right to demand the loaned shares back at any time. Thus one particular parcel of shares has procreated two “long” positions and each of the two buyers of that particular parcel of shares will receive a monthly brokerage statement indicating that that particular parcel of shares is being “held long” for them.

The b/d of the new purchaser of the shares needing a borrow from the SBP for his purchase transaction now has all of the right in the world to place that very same parcel of recently borrowed shares right into the very same lending pool at the SBP as if they never left in the first place. When that parcel of shares is chosen to “cure” another FTD on the next day there will now be three investors receiving monthly statements indicating that their b/d is holding this parcel of shares “long” for them. (Note that technically you can’t identify particular parcels of shares due to “anonymous pooling”. There are now 3 “co-beneficial owners” of that one parcel of shares.

But wait a minute since “CEDE and Co.” technically is the “legal/nominal/record” owner of all of those shares then it would be pretty tough for the 3 “co-beneficial owners” of that parcel of shares to ever learn these facts and then make a case for corruption at the DTCC. Remember that shares are held in an “anonymously pooled” or “fungible bulk” format at the DTC and the various DTCC participating technically own a “proportionate interest” in the shares that the DTC holds.

Imagine the abuses possible in a clearance and settlement system utilizing a self-replenishing SBP. Imagine also the responsibilities of the administrator of such a system to make sure that it doesn’t have any abusive participants selling nonexistent shares in an effort to access the self-fulfilling prophecy aspect of ANSS involving merely collateralizing the monetary value of a failed delivery obligation. If not monitored for abusive NSCC participants could easily place the share price of the corporation under attack into a “death spiral” which lessens the collateralization requirements which in turn allows an investor’s funds to flow to the party absolutely refusing to deliver that which it sold. Note that there are two issues here. Firstly, how in the world can a system like this be the system of choice unless somebody was looking after the financial interests of those that own and run the system? Secondly, if by some miracle this is the best design available then where is the rigorous program to detect and address abuses?

Can you imagine the cataclysm that could befall the investors in a clearance and settlement system if the administrator of such an SBP refused to monitor for these obvious abuses in order to further the financial interests of their bosses that own the NSCC? Picture for a moment the abuses available to securities fraudsters if the administrators of this SBP were to unconscionably proffer that they can’t do anything about this SBP “because it’s automated and they have no discretion in the matter”. That quote is from the NSCC’s contribution to an amicus brief filed by the SEC in a lawsuit filed by a corporation allegedly being attacked in an ANSS “bear raid”. The argument being proffered that the SBP is some form of automaton that admittedly shunts investor funds to the owners and administrators of the SBP that cannot do anything about this unfortunate circumstance is rather unique.

Is the NSCC aware of this “two sets of books” aspect to their clearance and settlement system? Of course they are; they’re the party administering the SBP and they’re also the CCP that is now acting as the surrogate creditor of the failed delivery obligation. Shouldn’t a prospective investor be made aware of the identity of certain corporations that have so many incredibly damaging “securities entitlements” resulting from SBP abuses that the invested in company has basically been preordained to an early death? Could any fact be of more of a “material” nature than this?

Some questions that arise might include the following. How can one parcel of shares give rise to so many “long” positions that are theoretically being “held” somewhere? In reality the securities being “held long” by a DTCC participant and as referenced on a monthly brokerage statement can refer to either real shares being held in a vault or mere IOUs being held on the books of a participant as a failure to deliver or failure to receive. In the example cited above with the 3 “co-beneficial owners” of the same parcel of shares which of the 3 gets to vote them at the next annual meeting?

The student of abusive naked short selling must recognize the “Ponzi” scheme aspect of the NSCC-administered SBP. In essence it “undoes” yesterday’s “delivery” of shares in order to “cure” today’s failure to deliver. Since “good form delivery” is needed to achieve the legal “settlement” of a trade the SBP basically “undoes” the settlement of yesterday’s trade in order to present the illusion that today’s trade settled. Recall that “good form delivery” cannot be achieved by borrowing shares out of a self-replenishing lending pool and thus none of these trades legally “settle”.

I’m not 100% sure if this “two sets of books” aspect of the DTCC and its participants is technically “illegal” or if the refusal to monitor for and address the abuses being encouraged is what’s “illegal”. Since the perpetration of these frauds is definitely “illegal” as per 10b-5 and the new 10b-21 of the “34 Exchange Act then perhaps it doesn’t matter. The intentional handcuffing of management from accessing the information regarding share structure that it needs to properly fulfill its fiduciary duties of care to its shareholders is definitely illegal.

Note that the above scenario was made under the assumption that there were no FTDs held in an “ex-clearing” format. The NSCC might have a slightly more valid excuse as to why they don’t monitor for abuses in FTDs held in “ex-clearing” arrangements. In reality however they, as an SRO or “self-regulatory organization”, are mandated to regulate the “business conduct” of its participants and it is their participants’ “business conduct” that is involved in these “arrangements” to procreate and later hide FTDs. In fact SROs are to play the role of the “first line of defense” against fraudulent behavior on Wall Street. Unfortunately for American investors the patchwork nature of our securities regulatory apparatus has enforcement gaps that amount to a “regulatory vacuum” and foremost amongst those is the one pertaining to abusive naked short selling (“ANSS) frauds.

I’m adjusting my rabbit ears on my tin hat.

Diane, look at Deutche Bank’s involvement in the failure of MJK Clearing in 2001 re: a daisy chain of shares bought and relent.

http://www.sipc.org/pdf/SIPC_dt.PDF

It’s should be a made for TV movie:

– Adnan Khasshogi, friend of president’s and international arms dealer behind it

– Valerie Redhorse, Michael Milken’s office manager and now up and coming actress behind it

– fails on September 11th, but not one mention on major news networks. Shares in 175,000 investor accounts at risk, bailed out by SIPF.

http://www.madcowprod.com/MC6812004.html

Do you know what would be really sweet? To come up with a way to determine which of Madoff’s victims truly got hoodwinked and which assumed that he was front running buy orders and wanted to benefit from someone else’s crime and then shunt any money recovered only to those that got hoodwinked.

Dr DeCosta,

You should gather up your latest posts and put them in your blog at thesanitycheck. That way we can retrieve them without having to search here in the blogs.

Was that “our” Bethany Mclean on the Daily Show last night explaining what caused the market to crash and not mentioning corrupt lapdogs or fails to deliver?

Sure was kevin….see video

http://www.thedailyshow.com/video/index.jhtml?videoId=215930

Jon gets it. He mentioned the corruption and the selling of uncollateralized bonds. He must be listening to Max Keiser.

http://news.yahoo.com/s/ap/20090116/ap_on_go_co/tax_havens

Report: Over 8 in 10 corporations have tax havens

By KEN THOMAS, Associated Press Writer Ken Thomas, Associated Press Writer – Fri Jan 16, 6:28 pm ET

WASHINGTON – Eighty-three of the nation’s 100 largest corporations, including Citigroup, Bank of America and News Corp., had subsidiaries in offshore tax havens in 2007, and some of the companies received federal bailout funding, a government watchdog said Friday.

The Government Accountability Office released a report that said Bank of America Inc., Citigroup Inc. and Morgan Stanley all had more than 100 units in countries that maintain low or no taxes. The three financial institutions were included in the $700 billion financial bailout approved by Congress.

Insurance giant American International Group Inc., which has received about $150 billion in bailout money, had 18 subsidiaries. JPMorgan Chase & Co. had 50 units and Wells Fargo & Co. had 18; both financial institutions received government bailout money.

Sens. Carl Levin, D-Mich., and Byron Dorgan, D-N.D., who requested the report, have pushed for tougher laws to fight offshore tax havens around the globe. Levin, who leads the Senate Permanent Subcommittee on Investigations, has estimated abusive tax havens and offshore accounts cost the U.S. government at least $100 billion a year in lost taxes.

“I think we should take action to shut down these tax dodgers and we will be introducing legislation to do just that,” Dorgan said.

General Motors Corp., which received $13.4 billion from the federal rescue package, had 11 offshore subsidiaries while GM’s financing arm, GMAC LLC, had two offshore units. GMAC, whose majority owner is private equity firm Cerberus Capital Management LP, received $5 billion from the Treasury Department in late December.

Citigroup said in a statement that it has more than 4,000 subsidiaries around the globe “which enables us to serve hundreds of millions of individuals and institutions in more than 100 countries.” A News Corp. spokeswoman declined comment. Messages were left with several of the companies identified in the report.

Separately, the GAO said 63 of the 100 largest federal contractors maintain subsidiaries in 50 tax havens.

Levin noted that many competitors use the tax havens to varying degrees. PepsiCo Inc. has 70 subsidiaries while the Coca-Cola Co. has eight units. Caterpillar Inc. had 49 while Deere & Co. had three.

“We need to put an end to the use of offshore secrecy jurisdictions as tax havens,” Levin said.

The GAO said the subsidiaries could be established in the countries “for a variety of nontax business reasons” and said having a business unit in one of the countries “does not signify that a corporation or federal contractor established that subsidiary for the purpose of reducing its tax burden.”

Citigroup had 427 units in 23 countries, including 91 subsidiaries in Luxembourg and 90 in the Cayman Islands. Morgan Stanley had 273 units, News Corp. had 152 and Bank of America had 115. Procter & Gamble Co. had 83 subsidiaries and Pfizer Inc. had 80 in the jurisdictions.

Several major corporations have announced plans to leave Bermuda, a leading offshore business center, amid the global financial crisis and fears of tighter tax rules. Tyco Electronics Ltd., which makes electronic components, and Foster Wheeler Ltd., an engineering and construction company, are reincorporating in Switzerland — which has a tax treaty with the U.S. — for tax and other reasons. Covidien Ltd., a health care products company, is heading to Ireland.

___

On the Net:

U.S. Government Accountability Office: http://www.gao.gov/

Collapse ArticleTurn OFF Expand/Collapse Article

ANALYSIS OF THE DTCC’S PLEA THAT THEY ARE “POWERLESS” TO BUY IN THEIR ABUSIVE PARTICIPANTS’ FAILURES TO DELIVER

We’ve pretty much established how easy it is for abusive DTCC participants and their co-conspiring hedge fund “guests” to establish massive naked short positions by simply refusing to deliver that which they sell. What could be easier? We’ve reviewed how a clearance and settlement system illegally incorporating a foundation of “collateralization versus payment” (CVP) instead of the congressionally mandated “delivery versus payment” (DVP) foundation which incorporates the “prompt settlement” of all securities transactions will result in the ability for those refusing to deliver that which they sell to still gain access to the funds of the investors they are stealing from.

After all, all they’re asked to do is to collateralize the monetary value of the resultant failed delivery obligation on a daily marked to market basis. As the share price of the corporation under attack predictably “tanks” from the amassing of readily sellable “securities entitlements” procreated by these intentional “failures to deliver” (FTDs) then lo and behold the unknowing investor’s money unconscionably flows to those refusing to deliver that which they sold. This stolen money can they be redeployed to assume and collateralize that much higher of a naked short position. The result is that the corporation targeted for attack is going down and bringing the investments made therein and the jobs that it used to provide with it. From the targeting phase onwards there is a self-fulfilling prophecy that can be easily accessed by merely refusing to deliver that which you sell.

With that in mind the obvious solution becomes to “buy-in” these intentional “refusals to deliver” (RTDs) or “failures to deliver” (FTDs) at a point in time when it becomes obvious that the seller of bogus shares has no intention whatsoever to deliver that which it is selling. Since some delays in delivery are legitimate then these must be provided for which results in the appropriate buy-in timeframe being somewhere around perhaps T+6 or T+7.

Now the question becomes which “market intermediary” to the transaction should be responsible for “executing” the buy-in. Make a mental note about the term “executing” as it will come up many more times again. Let’s once again review the DTCC’s now famous 1/27/06 press release:

”DTCC subsidiaries clear and settle trades. Short selling and naked short selling are trading strategies regulated by the marketplaces and the SEC. DTCC is involved after a trade is completed at the marketplace. DTCC does not have regulatory powers or regulatory responsibility over trading or to forcing the completion of trades that fail. As the SEC has stated, fails can be the result of a wide range of factors.”

As you can see the gist of this statement is that the DTCC is certainly not the party that should be executing these “buy-ins”. I beg to differ. Let’s take a look at the various roles that the DTCC and its DTC and NSCC subdivisions have volunteered to perform or have been mandated to play in our clearance and settlement system.

1) They act as the all-important “central counterparty” (“CCP”) to all trades by injecting themselves in between the buyer and the seller for reasons associated with enhanced efficiencies and the ability to provide a “trade guarantee” informing the world of how safe our markets are.

2) As the CCP they have accepted the incredibly tempting to abuse power to “discharge” the delivery obligations of any of their “participants” that fail to deliver that which they sell.

3) As the CCP they are then forced to “assume” these failed delivery obligations onto their own shoulders.

4) After “assuming” these delivery obligations they are then mandated to “execute” (here’s that word again) on these obligations so that the purchaser of the shares involved in the trade receives that which she or he paid for. Our clearance and settlement system is based upon the tricky legal concept of “novation” which means “to create anew”. Utilizing the legal concept of “novation” the original contract between the buying and selling party is “discharged” by the CCP and two new contracts are created or “novated”. The first involves the CCP’s “assumption” of the contract to receive the funds of the buyer and forward them onto the seller and the second one involves the “assumption” of the contract to receive the shares from the seller and then to forward them onto the buyer. What was the presumption involved here in this ultra-risky approval of allowing the CCP to “discharge” delivery obligations? It was that the CCP would ACT IN GOOD FAITH and “execute” on the delivery obligations that it just “assumed” especially keeping in mind that the original delivery obligation has already been “discharged”. IN ESSENCE THE PRESUMPTION MADE WAS THAT THIS CCP (THE NSCC) WOULD NOT HAVE THE AUDACTITY TO PLEAD TO BE “POWERLESS” TO BUY-IN THE DELIVERY FAILURE OF THE ORIGINAL SELLER IF HE ABSOLUTELY REFUSED TO DELIVER TO THE NSCC THAT WHICH IT SOLD. If the original seller refused to deliver that which it now owes to the NSCC as the CCP then how else can the NSCC forward the missing shares on to the buyer unless he plays “hard ball” with any participant refusing to deliver to this intermediary (the NSCC) that which it sold especially keeping in mind that the original delivery obligation has been “discharged”. In other words what might happen if the NSCC management would refuse to act in good faith by failing to “execute” on the delivery obligations it just “assumed” on behalf of the financial interests of its employers which include the abusive “participant” that refuses to deliver that which it sold. After all, acting contrary to the financial interests of your bosses presents a rather slippery slope.

5) The nominee of the DTCC (“CEDE and Co.”) has volunteered to act as the surrogate “legal/nominal/record” owner of all shares held in “street name”. Why does the clearance and settlement system need a centralized “legal/nominal/record” owner to act in this surrogate capacity? It is because it circumvents the tremendous amount of paperwork that would otherwise be involved in executing “deedlike” instruments every time a trade is executed. What was the assumption made in placing a “surrogate” owner in this capacity? The presumption made was that the “participants” making up this surrogate owner would ACT IN GOOD FAITH in this incredibly powerful and easily abusable role that could easily be “leveraged” against the investors for whom the surrogate owner now represents. After all, in our legal system the “legal owners” of any form of private property can pretty much do anything they want with their “possession”. There was a gigantic leap of faith taken in this regard. Can you imagine the cataclysm for investors if this party assuming these delivery obligations and responsibilities associated with acting as the surrogate owner of all shares held in “street name” refused to act in good faith in order to further the financial interests of the owners of the DTCC their bosses?

6) Acme’s transfer agent, registrar, management team and shareholders have also “entrusted” the DTC subdivision of the DTCC to act as both the legal “custodian” of their shares held in “street name” and to administer the “depository” for these securities to have rigorous checks and balances in place to thwart any efforts to “counterfeit” these securities. The legal “custodian” of these shares cannot administer a self-replenishing SBP which openly counterfeits that being held in its “custody”. The analogy would be to keep the vault unlocked and allow their abusive participants to gain access and photocopy the stock certificates that they act as “custodian” for. Anti-counterfeiting efforts are usually the purview of a company’s transfer agent and registrar but when almost all shares are held in “street name” by “CEDE and Co.” these professionals are literally blinded in their effort to detect and address any efforts to counterfeit what is held in “street name”. The shareholders of a corporation have “entrusted” the DTC to perform in this regard since their transfer agent has been blinded. Once again the presumption was made that the DTC would ACT IN GOOD FAITH in this incredibly powerful and easy to abuse role.